Wall Street ended the week decisively weaker as an extraordinary oil shock collided with mounting war risk in the Middle East. The situation forced investors to quickly reprice inflation and growth assumptions.

WTI crude surged more than 36% on the week, posting its largest weekly gain since futures began trading in 1983 and briefly topping USD 92.60, while Brent crude briefly topped USD 94.50. The effective disruption to traffic through the Strait of Hormuz has shifted the narrative from “tight supply” to an “availability crisis,” as tanker owners balk at running the gauntlet of missiles and drones despite new U.S. re‑insurance facilities.

Treasury yields responded sharply, with the 10‑year up about 4.6% on the week, the 2‑year up 5%, and the 30‑year up 3.2%, as bond markets adjusted to higher and potentially stickier inflation expectations. Headline nonfarm payroll shocked with a 92k decline against expectations for a 60k gain, hinting at a cooling labor market.

The US Dollar Index (DXY) surged but failed to hold above the January high of 99.4. Oil exporters benefited, particularly the Canadian dollar, which gained nearly 2% against the Euro in a single week.

Pairs In Focus

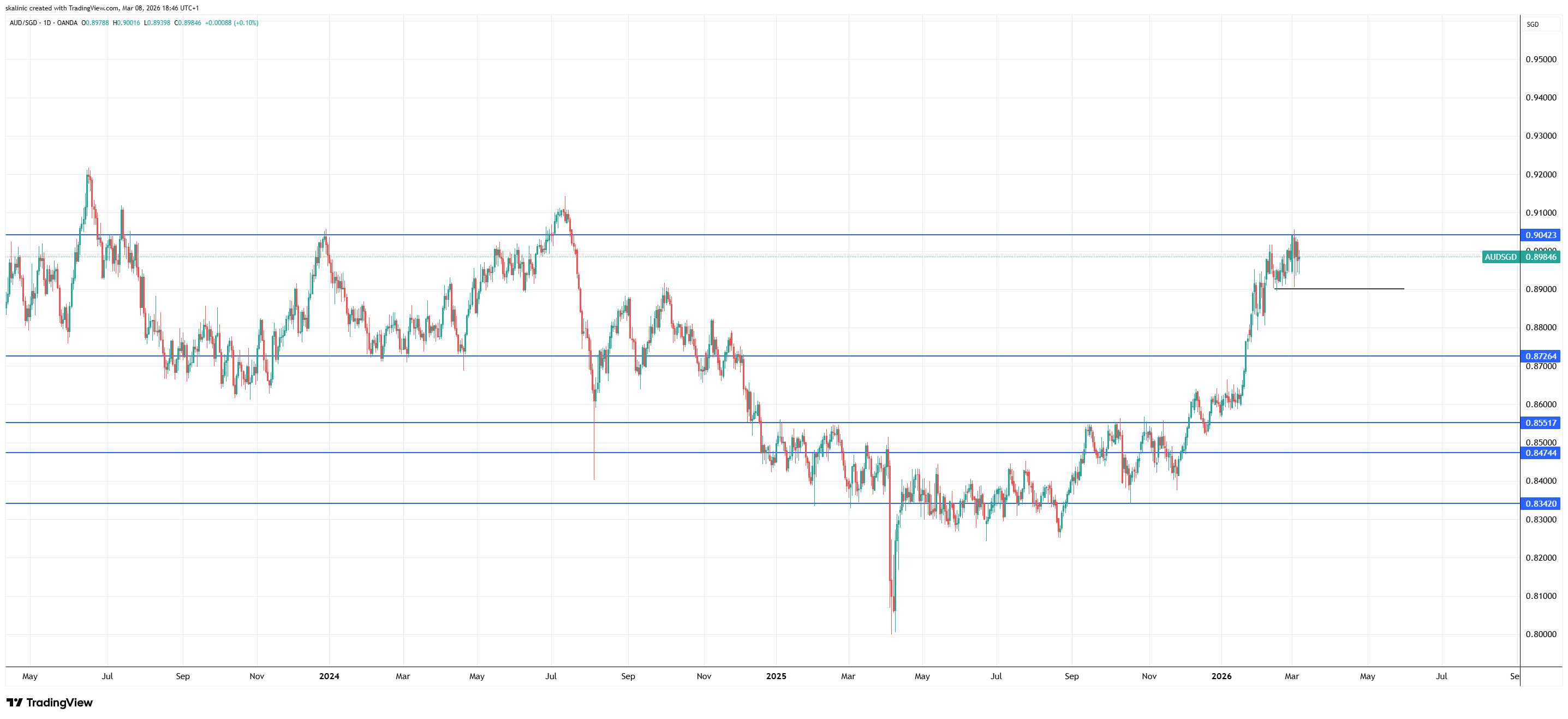

AUD SGD

This pair has touched the resistance around 0.9042 but has so far rejected the first attempt to break through. However, given the persistent strength of the AUD as a commodity currency, as long as 0.89 support holds, the possibility of a breakout gets stronger.

AUD/SGD Daily Chart, Source: TradingView

The potential upper targets are highs from July 2024 and June 2023.

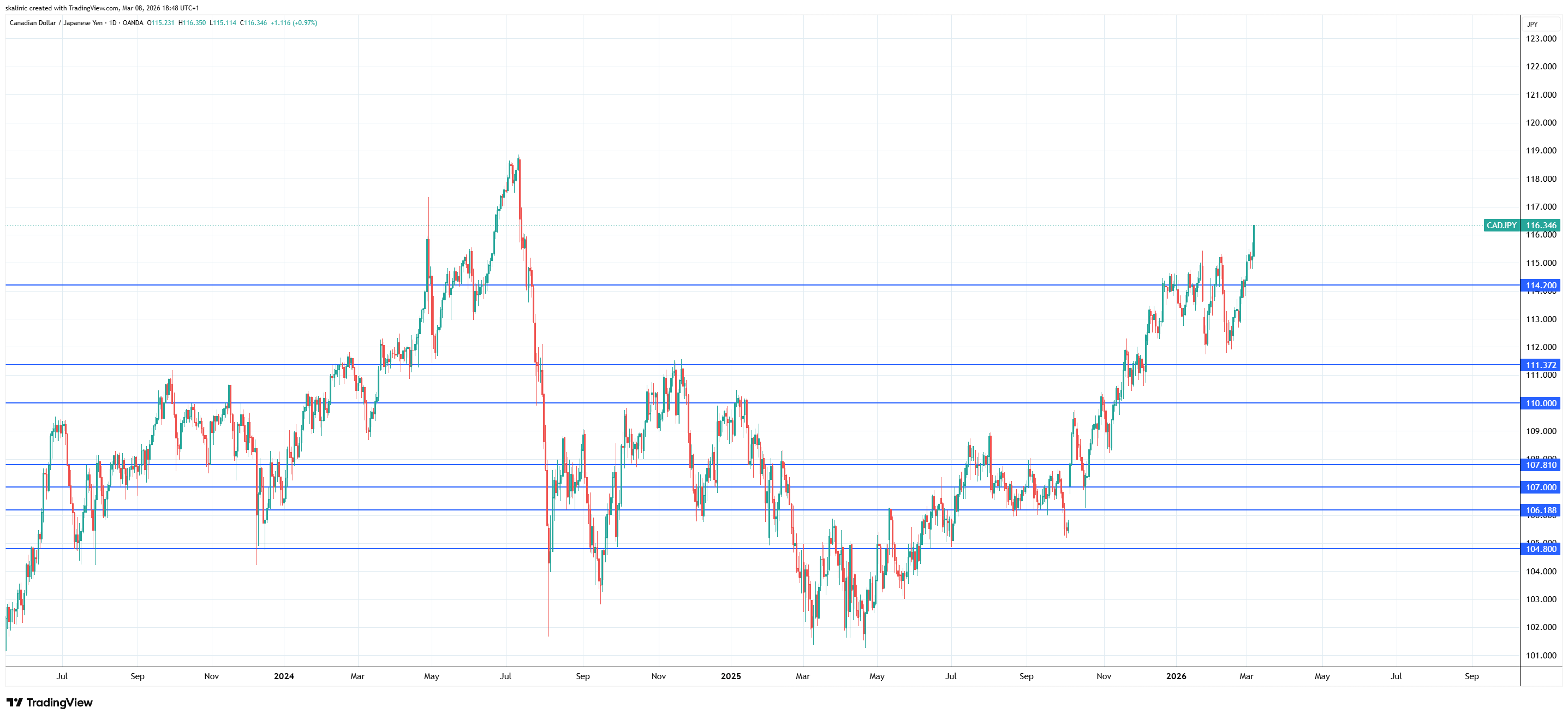

CAD JPY

The Canadian dollar is among the strongest currencies right now, owing to its meaningful correlation with oil prices. As long as conflict in the Middle East persists, the upside trajectory should continue.

CAD/JPY daily chart, Source: TradingView

A good short-term target to watch for is high from July 2024, at around 118.800.

Looking Ahead

The week ahead will revolve around whether the oil‑led inflation shock forces the Federal Reserve to lean more cautiously on rate cuts or whether weakening labor data and any softening in core price measures allow policymakers to look through the energy surge.

Wednesday’s February CPI is in focus, with consensus expecting both headline and core to be roughly 2.5% y/y. Any upside surprise, especially if driven by spillovers from higher transport and goods prices rather than just direct energy, would validate the recent back‑up in yields.

Friday’s core PCE, alongside January income and spending, will offer an even clearer read on underlying inflation momentum and consumer resilience. If both CPI and core PCE come in hot, the market narrative will likely shift toward “higher for longer, later cuts,” putting further pressure on rate‑sensitive sectors and supporting the US dollar against low‑yielding and energy‑importing currencies.

Alternatively, a benign inflation profile combined with evidence that household demand is cooling would revive the case for mid‑year easing and could cap the recent rise in yields, taking some steam out of the Dollar rally and easing pressure on equities outside the most energy‑intensive segments.

Until there is either visibility on de‑escalation in the Gulf or clear evidence that the inflation impulse can be contained without derailing growth, investors should expect a market biased toward stronger energy, firmer yields, and the dollar, and more fragile valuations in industrials, transport, and other energy‑sensitive risk assets.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.