The US Dollar ended last week under broader pressure, despite U.S data showing a positive mix of resilient growth, gradually moderating inflation, and a somewhat strengthening labor market.

January CPI slowed to 0.2% m/m versus 0.3% expected, reinforcing the narrative that disinflation is still inching forward. Nonfarm payrolls surprised to the upside with a 130k gain vs 70k consensus. In past cycles, that combination of solid jobs and cooling price momentum might have supported the USD, but this time, forex markets were more focused on the sharp drop in U.S. Treasury yields and evolving global flow dynamics.

The 10‑year slid hard toward the 4.05% area, a move far larger than the marginal shift in Fed pricing, as investors sought duration amid ongoing de‑risking in other asset classes and lingering concerns about tech valuations and crypto volatility. This compression in long-end yields weighed on the US dollar despite only modest changes in expectations for the first rate cut; March is now almost fully priced as a hold, and June odds for easing have edged only slightly lower. Given these dynamics, the short-term US Dollar rally remains as a correction within the broader downtrend, rather than a full-blown trend reversal to the upside.

The AUD continued to benefit from a hawkish RBA tone, while the Yen extended its recent outperformance even as Japanese equities surged to new records following Prime Minister Sanae Takaichi’s landslide election victory. That rare alignment of a strong Nikkei index and a firmer Yen signaled that markets are temporarily rewarding Japan for political clarity and perceived fiscal discipline, breaking the usual pattern where risk-on in Japanese stocks goes hand in hand with JPY weakness.

Pairs In Focus

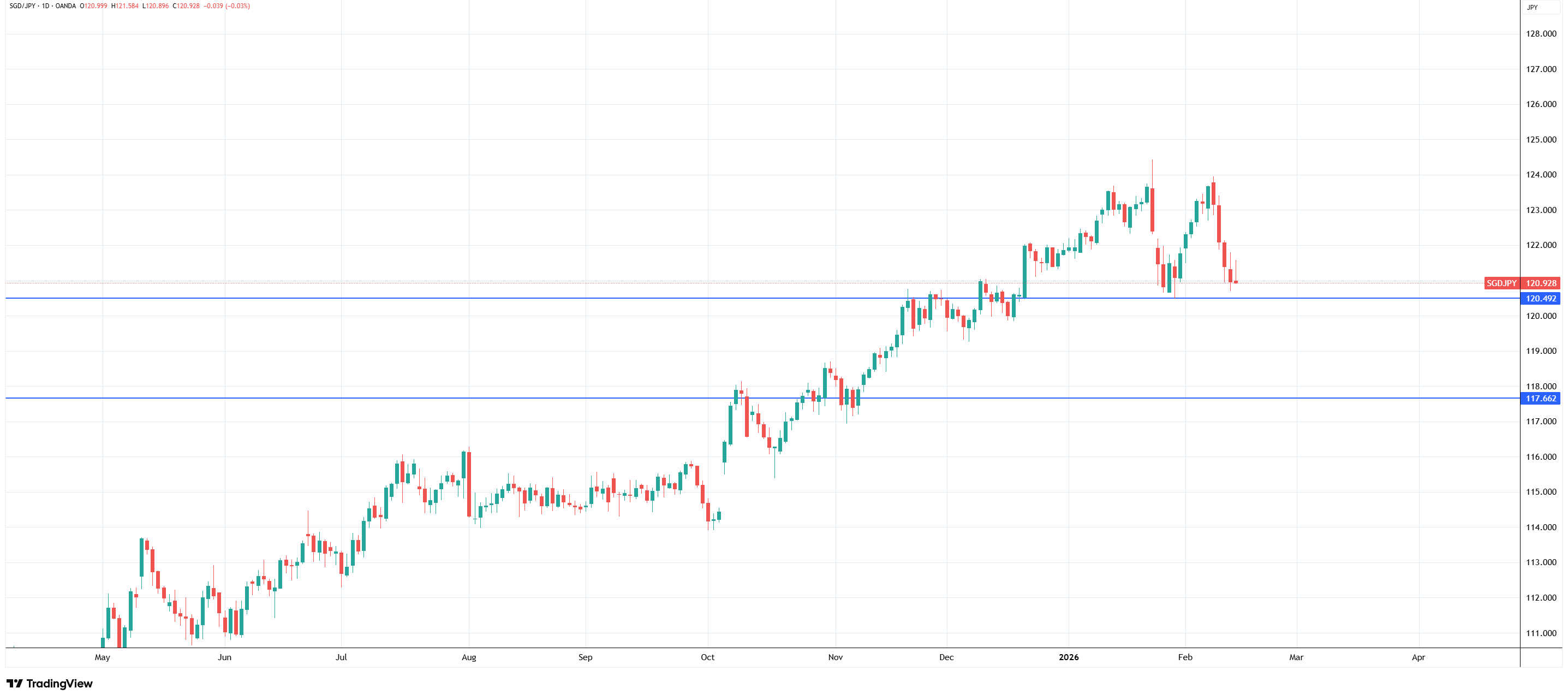

1. SGD JPY

The yen's strength is evident in the chart's technicals. Against the SGD, it made a marginally lower high and is now pressuring the former resistance that has turned to support.

SGD JPY daily chart, Source: TradingView

If price breaks and stays below 120.500, the odds of a further downside slide grow exponentially. The key level to watch then becomes 117.660.

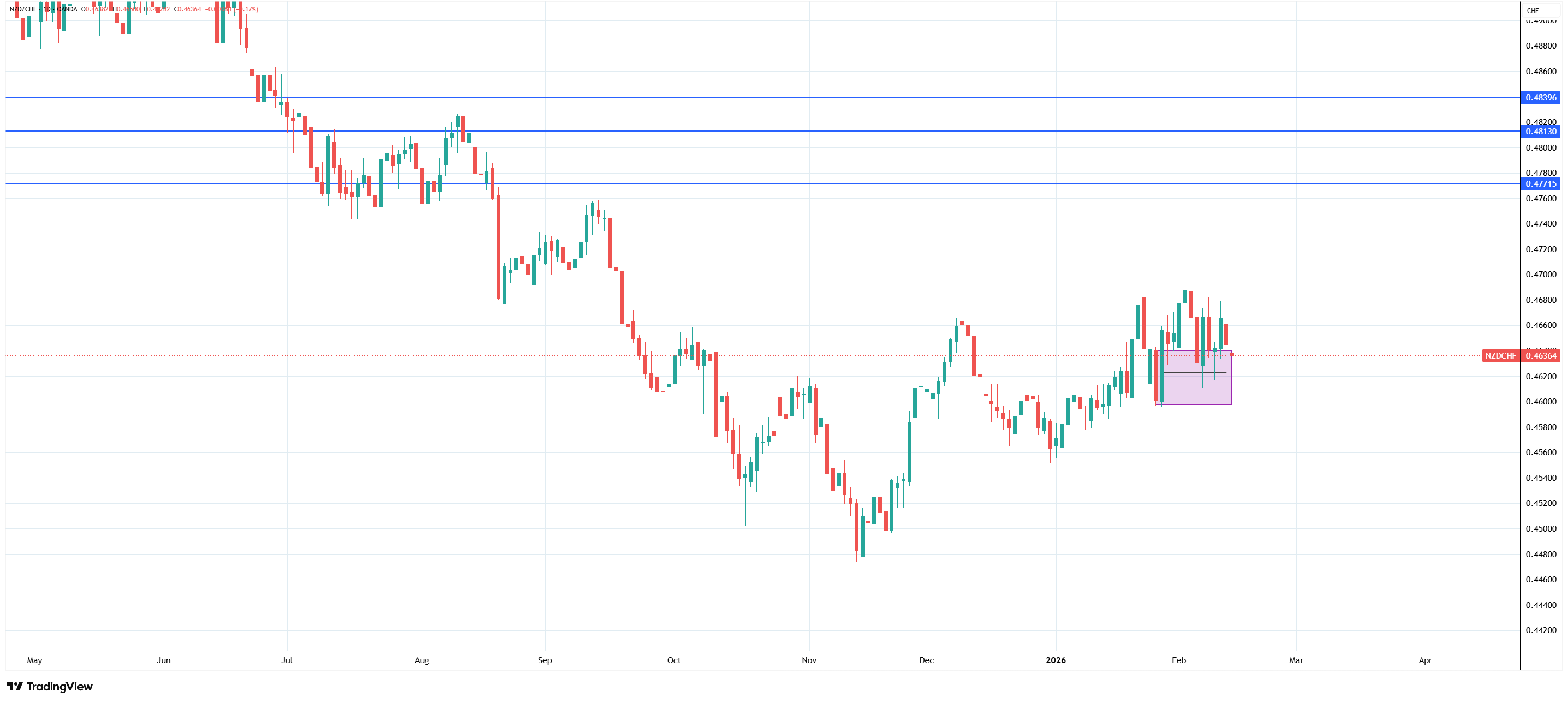

2. NZD CHF

This pair is still flirting with a trend reversal, but as the pullback unfolds, that chance is becoming smaller.

NZD CHF daily chart, source: TradingView

The level to watch is 0.46200, and a round-number support level is below at 0.46. If that level breaks, the likelihood is that the trend to the downside will prevail.

The Week Ahead

The shorter week ahead features a lighter U.S. data calendar. However, a cluster of late-week catalysts might decide whether the US dollar’s weakness accelerates. The attention will be on Wednesday’s FOMC minutes and Thursday’s jobless claims.

Those data points might provide additional clues on how firmly the Fed is committed to staying on hold. Friday’s preliminary Q4 GDP, alongside December income and spending, will be critical for gauging whether consumer momentum is cooling enough to justify mid‑year easing or if the current pricing of cuts remains too optimistic.

For FX, a further slide in the 10‑year toward the 3.95–3.95% band would likely keep DXY on the back foot and could extend support to high‑beta currencies, including AUD, provided risk sentiment holds together.

Any rebound in yields back through the 4.17% area, especially if paired with firmer spending and income data, would open the door to a tactical Dollar bounce, particularly against low‑yielders like Yen and Franc. In Japan, with the election outcome now fully priced, the key question is whether the recent Yen–equity decoupling persists; a consolidation or pullback in the Nikkei from stretched technical levels could quickly reignite haven demand for JPY and cap any nascent USD recovery.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.