Wall Street lost steam last week as markets grappled with widening policy uncertainty, which went well beyond Greenland. While earnings continued to drive stock-specific volatility—notably Intel's 17% plunge—the broader narrative was one of investor fatigue with U.S. policy reversals and an expanding range of potential escalation points.

Gold extended its rally, climbing 8.5% amid intensified safe-haven demand amid geopolitical tensions and lingering concerns over Federal Reserve independence. However, the biggest development was the US dollar’s sharp underperformance across the board. It had the worst week in months, with losses exceeding 3% against both AUD and NZD, approaching 3% versus CHF, and nearing 2% against EUR and GBP.

This weakness was not driven by traditional catalysts, as economic data remained relatively resilient. Fed rate expectations barely moved, and equity indices stayed largely confined within prior ranges. Instead, the move reflected a growing policy risk premium being priced directly into U.S. assets, with the Dollar serving as the primary release valve for investor unease.

Trump administration threats of tariffs against Canada over its China trade deal, combined with reports of a potential oil blockade on Cuba, expanded the perceived range of U.S. policy options and normalized ideas previously considered tail risks. NZD and AUD excelled, as domestic data revived rate-hike speculations, while CHF followed closely.JPY rebounded on suspected government intervention, with USD/JPY drawing a line near 160, though the sustainability of the move depends on whether equity weakness reinforces the rally or reverses it.

Pairs in Focus

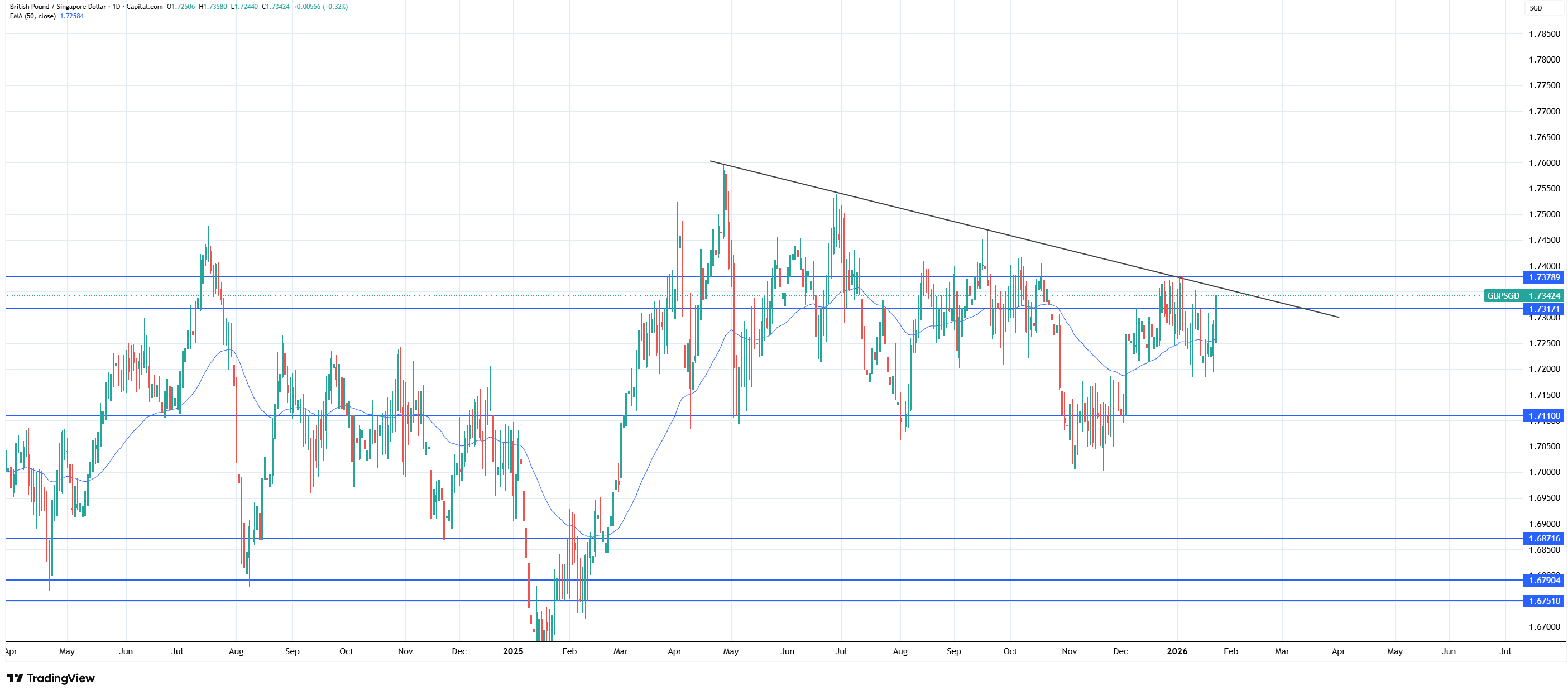

1. GBP SGD

The pound has broken the old key level at 1.73170 and is threatening to break the upper trendline. A key level to observe is 1.73790.

GBP/SGD daily chart, Source: TradingView

A clean break, a close above, and a subsequent retest could signal a fresh run at the previous year's highs.

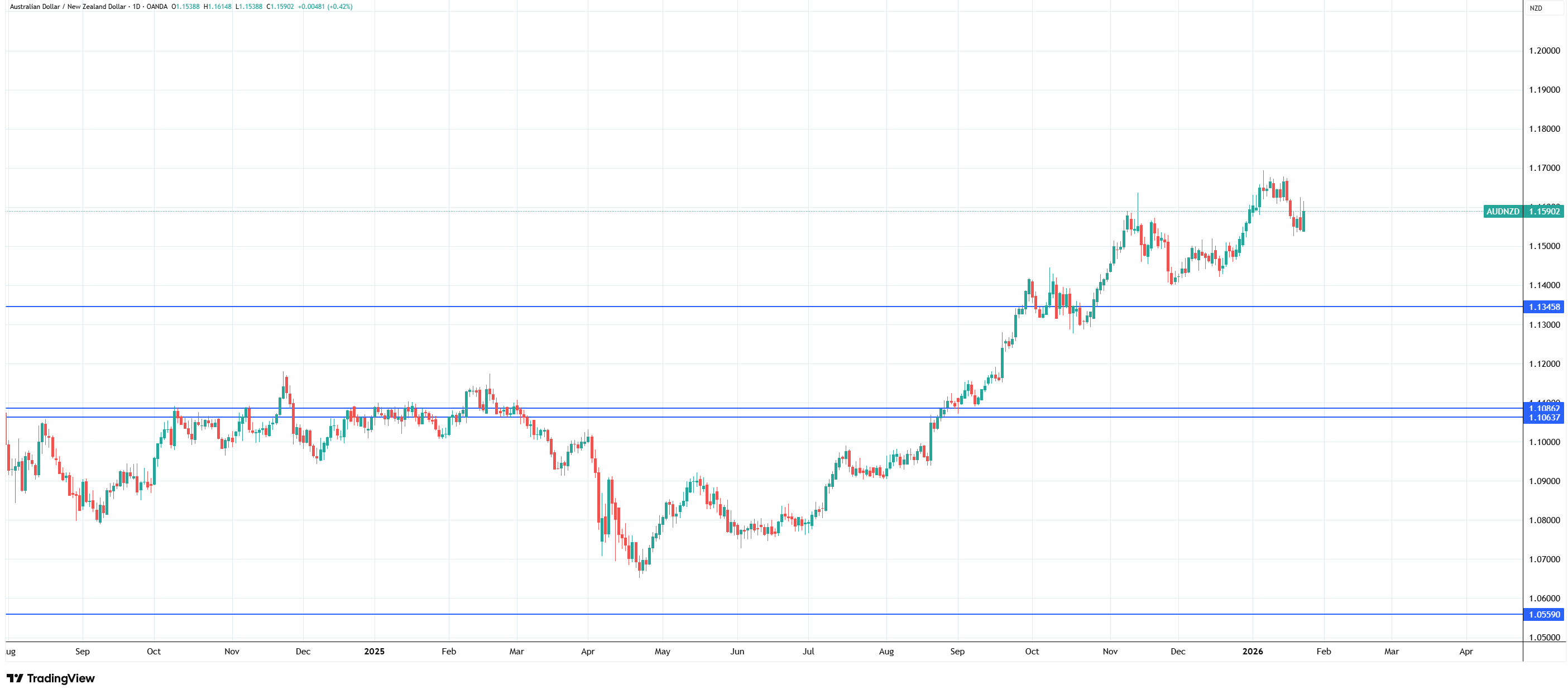

2. AUD NZD

Both AUD and NZD had a stellar recent run, but AUD fared comparatively better. It broke a long-term consolidation that anchored it near 1.10 and is now trading close to 1.16.

AUD/NZD daily chart, Source: TradingView

Technically, as long as it stays above the short-term support at 1.15500, a possibility for a continuation up remains solid.

Looking Ahead

The week ahead brings Big Tech earnings and a Federal Reserve decision that will command market attention. Apple, Microsoft, and Meta will offer crucial signals on the future of the AI market.

Powell’s press conference will draw attention to clues on easing timing, though rate expectations remain stable, with June still seen as the first realistic cut window. The critical question is whether Dollar's recent weakness hardens into a sustained rotation out of U.S. assets or proves merely a sharp warning shot.

The technical picture suggests further downside risk, with a break below 96.84 potentially accelerating the fall toward the 96.21 support and beyond, threatening the long-term uptrend channel that has defined Dollar strength since 2008. Yen's trajectory will be equally important; if Japanese equity weakness reinforces Yen appreciation, a feedback loop could emerge that amplifies both currency strength and financial tightening.

Meanwhile, any fresh policy escalation—whether on tariffs, Cuba, or other fronts—could reignite the "Sell America" trade and push investors further toward diversification away from U.S. assets, a theme that may define currency markets throughout 2026.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.