The US dollar ended last week softer but not directionless. Currency markets were influenced by shifting inflation signals, rising Treasury yields, and steady uncertainty surrounding the Federal Reserve and the White House.

Core CPI undershot expectations while PPI came in line, delivering a mixed inflation picture that did little to move the dial on the Federal Reserve’s near‑term policy stance. Yet despite softer data that normally would weaken the greenback, currencies reacted more to the structural recalibration underway across U.S. rate markets.

The late‑week breakout in the 10‑year yield, pushing decisively above the 4.2% barrier, signals a possible turn higher in long-term US yields. Even with this development, the dollar struggled to gain traction, held back by resilient equity sentiment and investors’ readiness to rotate into higher‑beta FX as geopolitical fears around Iran faded.

The New Zealand dollar led the G10, as revived manufacturing supported strong domestic data. The Canadian Dollar shared second place with the USD as optimism around renewed China trade engagement helped stabilize the CAD. European currencies fared poorly, with the Euro the weakest major, followed by the Swiss Franc and the Sterling, as political noise surrounding the Greenland dispute added to already flagging growth momentum.

Yen traded unevenly, supported at times by speculation over joint U.S.–Japan FX intervention and expectations of further BoJ tightening, but capped by the broad risk appetite that continued to dampen demand for safe havens. Meanwhile, the Dollar Index remains in a corrective up‑leg, though the muted response to the yield surge points to it being tied to equity performance and the broader risk cycle.

Pairs In Focus

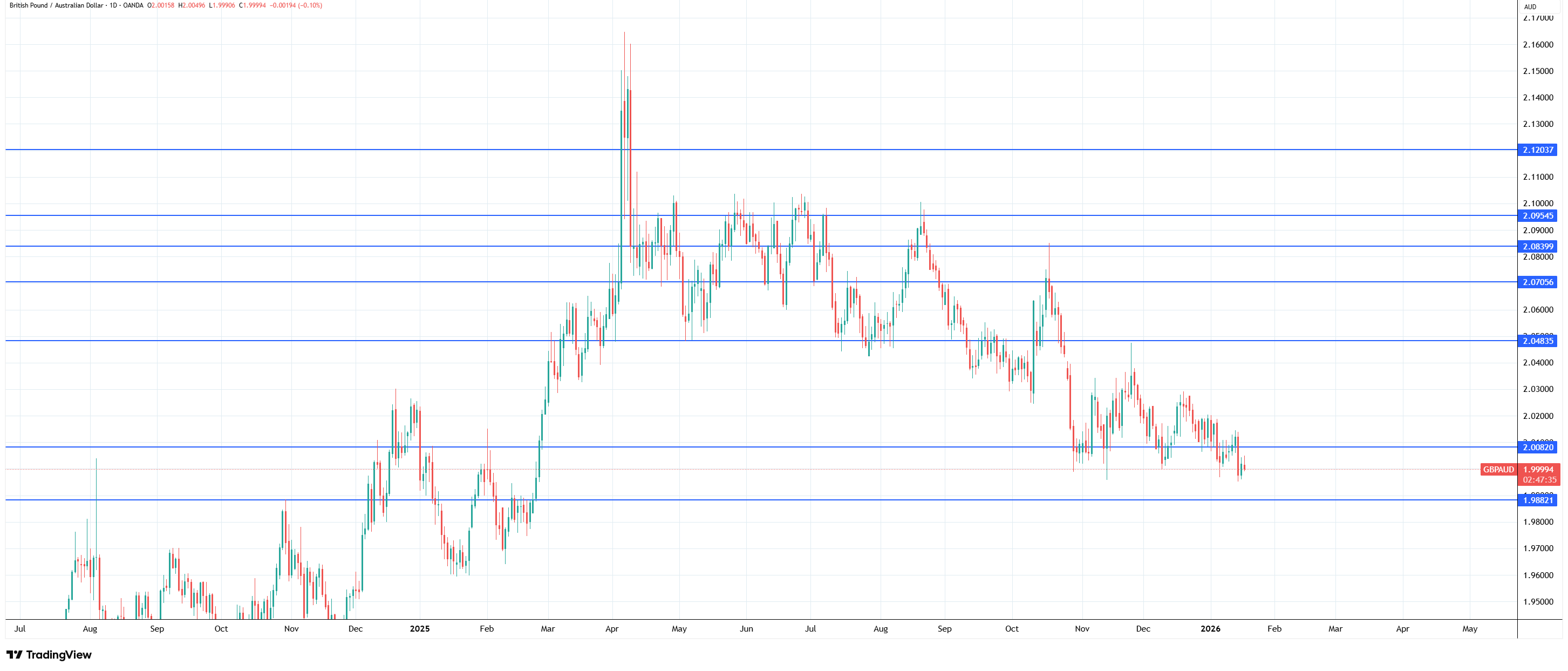

1.GBP/AUD

GBP/AUD has decisively weakened after struggling to break the trend in late November.

GBP/AUD Daily chart, Source: TradingView

Current indications are only for the trend to continue lower and eventually test the key level of 1.98820.

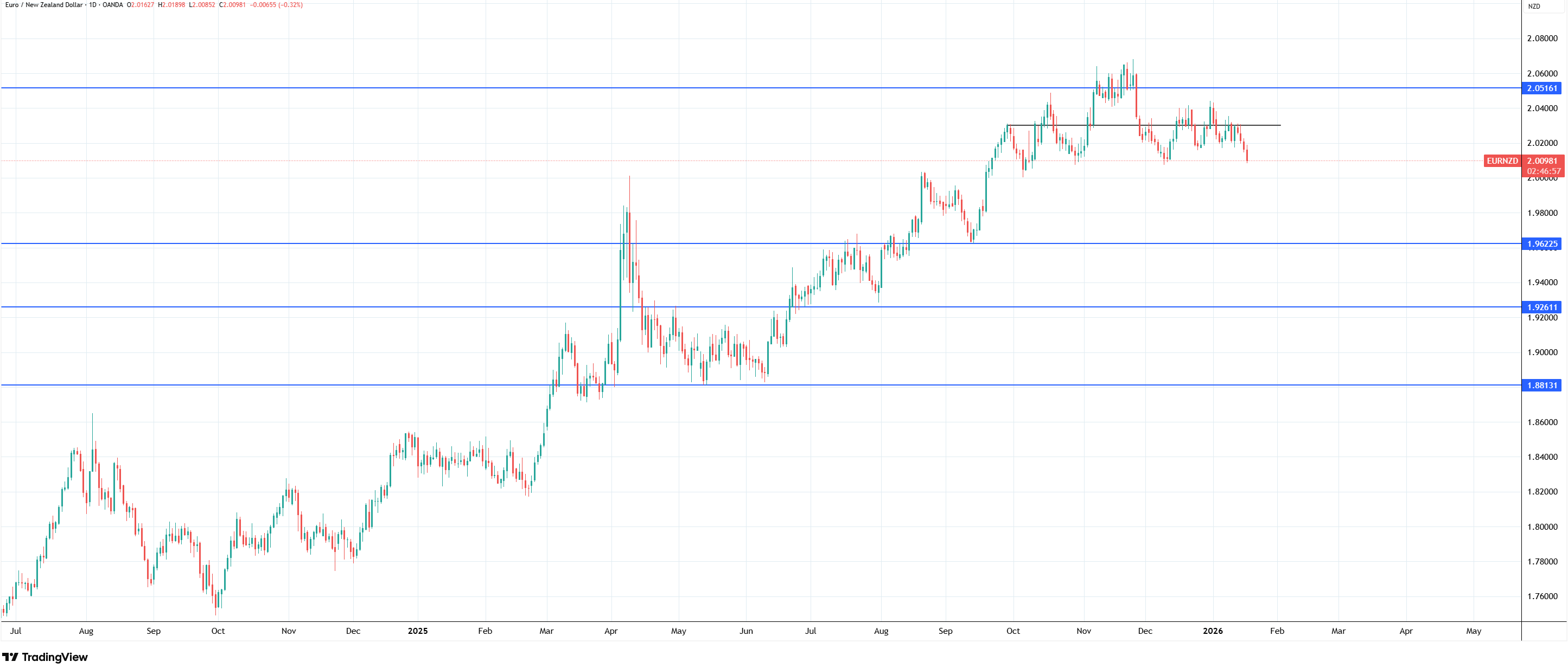

2.EUR/NZD

EUR/NZD peaked in November and has since formed a head-and-shoulders pattern with a baseline around 2.007.

EUR/NZD Daily Chart, Source: TradingView

A break of the baseline would mean a potential move down of nearly 3%, taking the price to test the previous key level at 1.96225.

Looking Ahead

This week might be shorter for a day, but there is no shortage of catalysts for the FX markets. Davos will dominate global headlines, with U.S.–EU tensions over Greenland likely to create intermittent headline volatility for the Euro and the Swiss Franc.

Equity earnings season is accelerating with results from Netflix, Intel, and major industrials, shaping risk sentiment and thereby the trajectory of Dollar‑sensitive carry trades. The delayed U.S. income and spending data for November and December will also be key, providing insight into whether softer inflation is feeding through to consumption.

With the 10‑year yield now above 4.2%, currency traders will be watching closely to see if the breakout extends toward 4.37% or fades back toward support—an outcome that could decisively influence whether the Dollar resumes its climb or stalls once more against improving global risk appetite.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.