The latest bout of market volatility once again originated outside of the traditional macro channels. Economic data remained consistent with a cautious Fed on an interest rate pause, while treasury yields remained within familiar ranges.

However, institutional shock arrived with Kevin Warsh’s nomination as Fed chair, forcing investors to reassess the policy and the institutional risk premium embedded in U.S. assets.

Precious metals provided the starkest illustration of that unwind. Gold spiked to nearly $5,600 and silver above $118 before both reversed violently, shedding more than 13% and roughly 30% from their respective highs as the “institutional decay” narrative priced into hard assets was partially walked back.

Yet currency markets told a more nuanced story. Dollar staged a late-week rebound, helped by Friday’s DXY strength and some stabilization in yields, but still finished as the weakest major over the week. Losses were broad-based, with EUR and GBP also underperforming, while NZD led gains, closely followed by AUD and CHF.

Capital quietly rotated away from the most U.S.-centric exposures and into a mix of higher‑beta and defensive currencies. USD/JPY and USD/CAD ended mixed, caught between domestic stories. It was suspected Japanese intervention lines near 160 in USD/JPY and Canada’s political friction with Washington, on one side, and global portfolio rebalancing on the other.

Technically, Dollar Index remains under medium-term pressure: the series of lower highs below the 101–102 region, combined with breaks of key supports, keeps the long-term risk skewed toward a deeper reassessment of the post‑2008 uptrend.

Pairs In Focus

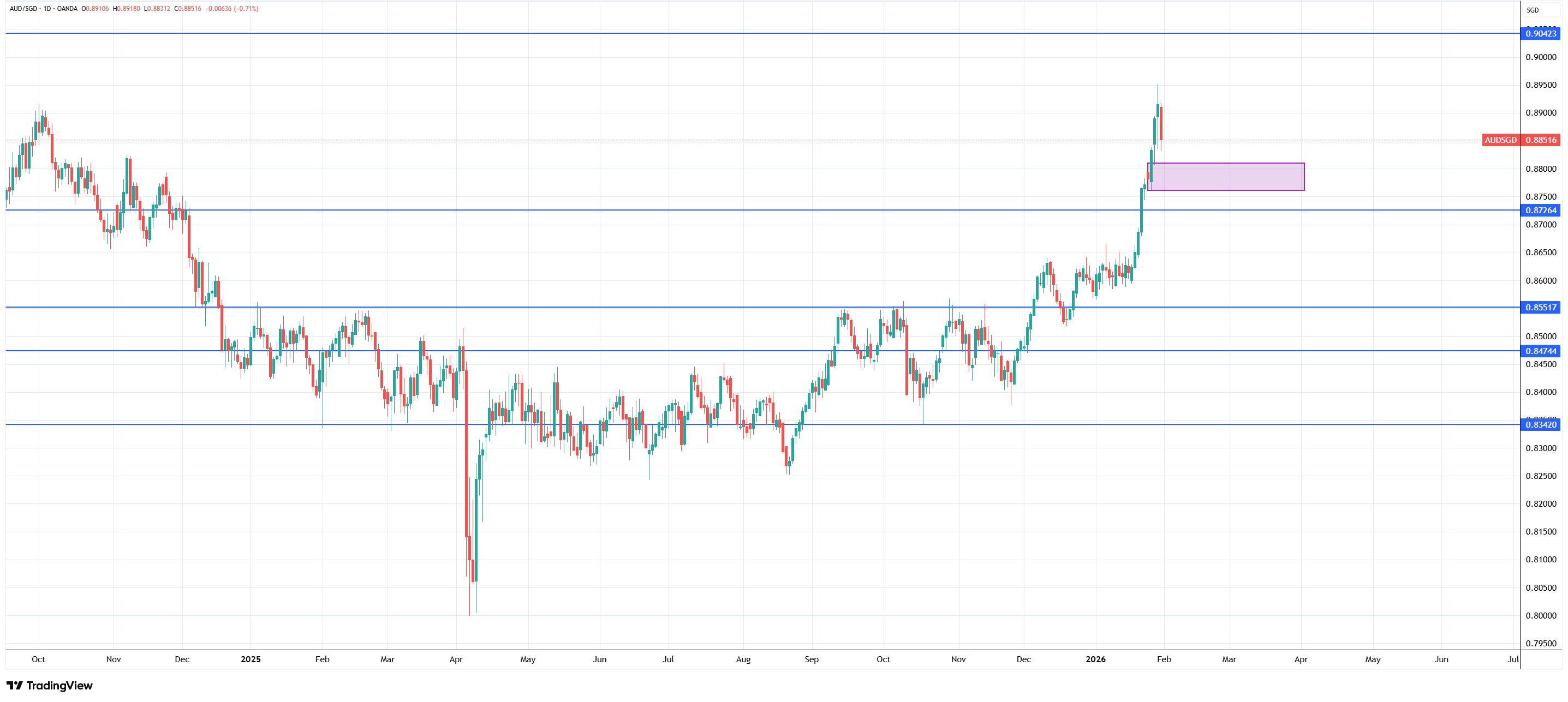

1. AUD SGD

This pair has strengthened, staging a decisive breakout through 0.86500 resistance. While it ended last week on a pullback, a dip toward a zone below 0.88000 would be a natural support point before the next potential leg up toward the 0.90423 target level.

AUD/SGD daily chart, Source: TradingView

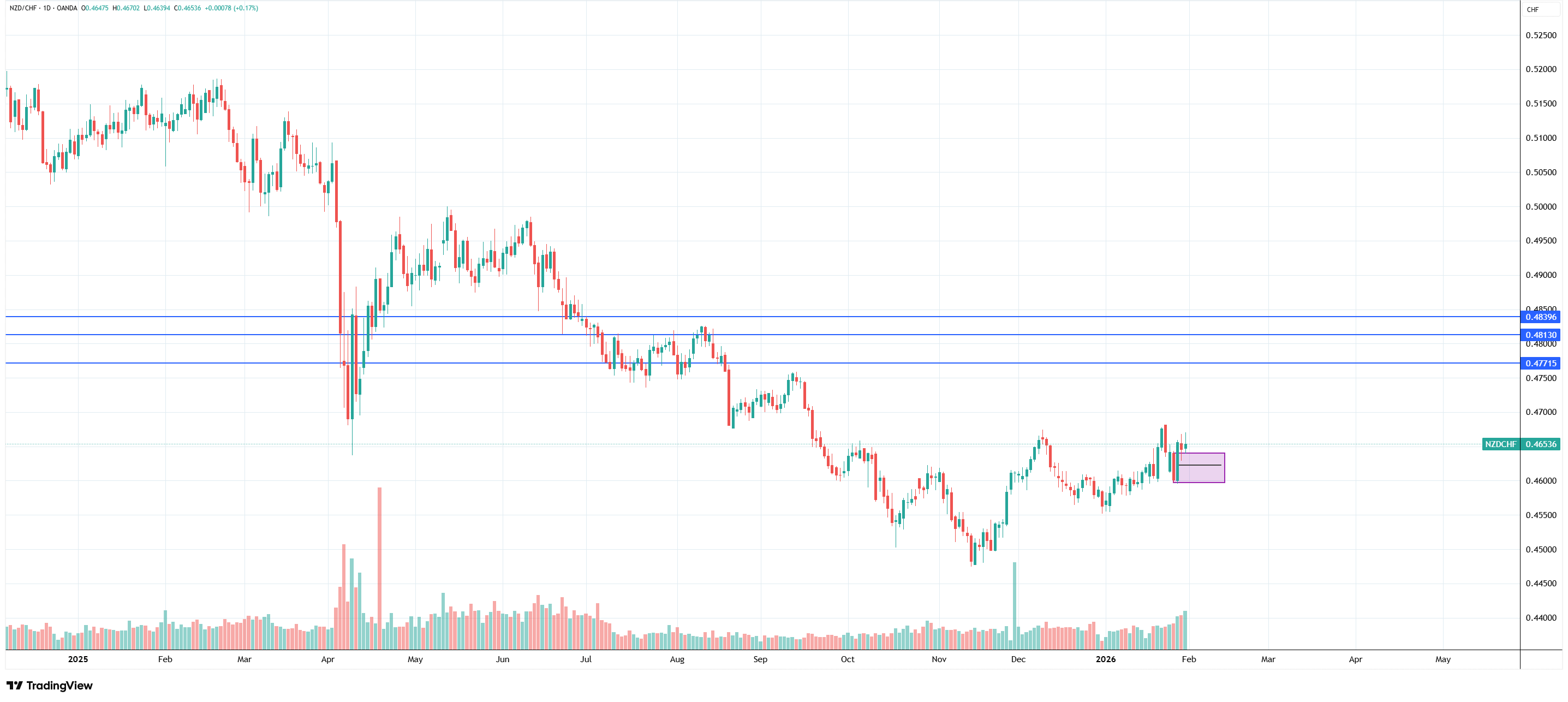

2. NZD CHF

NZD/CHF has created a higher low and a marginal higher high, staging a potential rebound after an entire year in a bearish trend.

NZD/CHF daily chart, Source: TradingView

To support this thesis, short-term price action should hold and not close below 0.46000, which was the latest swing low. If that level holds, the odds grow of rallying toward 0.47500.

The Week Ahead

The week ahead puts currencies squarely at the crossroads of macro data and mega-cap earnings. A dense U.S. data slate—S&P Global and ISM manufacturing surveys, JOLTS job openings, ADP private payrolls, services PMIs, weekly claims, and Friday’s Nonfarm Payrolls and unemployment rate—will test whether the Fed can credibly stay on hold without re‑igniting rate‑cut speculation.

Any downside surprise in labor or a clear softening in demand indicators would likely cap DXY’s nascent rebound and support high‑beta FX such as NZD and AUD. Alternatively, a resilient set of prints, combined with still‑contained jobless claims, would reinforce the case for higher‑for‑longer policy and could finally give the Dollar some follow‑through against EUR and GBP, especially as political noise around Greenland, Canada, and Cuba continues to weigh on European and North American peers.

RBA is expected to hike by 25 bps, bringing the rate to 3.85% from 3.60%, while the Bank of England and the ECB are expected to keep rates at 3.75% and 2.15%, respectively.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.