Wall Street ended the week sharply lower as the Middle East conflict continued to seep into the macro backdrop, driven by persistently high energy prices and a tightening of financial conditions. Brent gained about 8.9% over the week to settle around $112, while WTI slipped modestly to about $98, but both remain dramatically higher than a month ago, up roughly 55% and 47% respectively—enough to keep inflation anxiety elevated even when spot prices pause.

The Fed’s midweek decision to hold rates steady at 3.50%–3.75% for a third straight meeting was widely expected, yet the message mattered: policymakers explicitly highlighted uncertainty from the conflict as a drag on the outlook, reinforcing the sense of a “hawkish wait” rather than a pivot toward easing. That caution looked increasingly justified as inflation data surprised to the upside again, with February PPI printing at +0.7% m/m versus +0.3% expected, and core PPI at +0.5% versus +0.3% consensus.

Rates markets reacted accordingly, pushing yields higher across the curve: the 10-year rose to about 4.39%, the 2-year to 3.91%, and the 30-year to 4.94%. The equity tape struggled under this combination of energy-driven cost pressure, higher discount rates, and lingering geopolitical stress, with the S&P 500 down 1.9% and both the Nasdaq and Dow off about 2.1%. In FX, the surprise was not that markets were defensive, but that the Dollar failed to capitalize.

Despite risk-off conditions and rising U.S. yields that would normally lift USD, the greenback lagged as policy divergence took center stage: markets increasingly believe the ECB and, to a lesser extent, the BoE may be forced into a more aggressive stance to counter an energy shock that hits Europe asymmetrically. That re-pricing supported EUR and kept USD offered, leaving the Dollar Index to retreat but still above key support around 98.5—an uneasy stalemate between a waning rate advantage on the margin and episodic haven demand.

Pairs in Focus

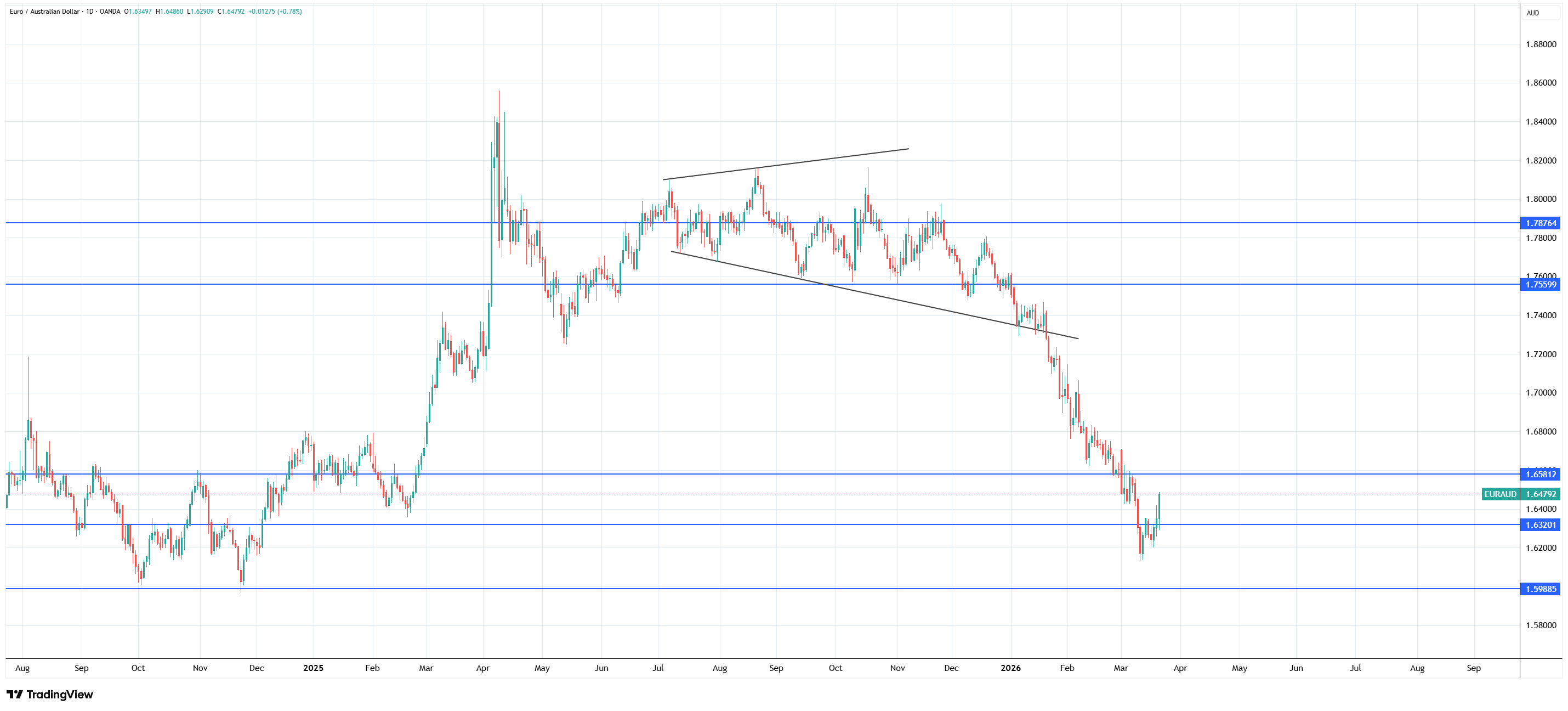

1.EUR AUD

This pair has shown some signs of bottoming, although it would be premature to declare a victory for the bulls.

EUR AUD Daily Chart, Source: TradingView

The level in focus remains 1.65800, and a break and retest of this level is one to watch for a meaningful short-term reversion to the upside.

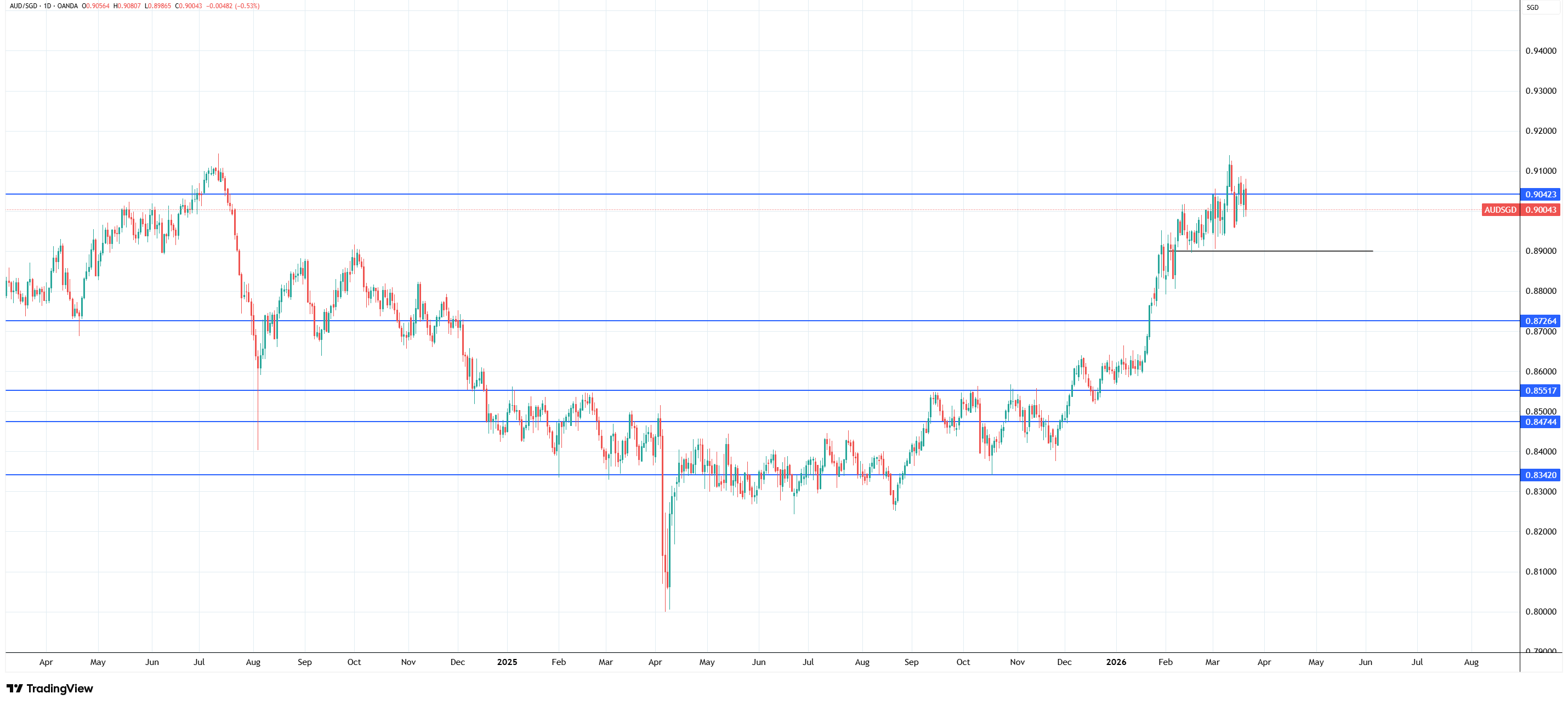

2.AUD SGD

After a strong bullish start to the year, AUD SGD ran into resistance at the previous year’s highs.

AUD SGD Daily Chart, Source: TradingView

The technical setup is for it to either do one of these two things: break above 0.91 and overcome this strong resistance. Or, decline to 0.89 and test the previous support.

The Week Ahead

The coming week will test whether that USD underperformance is a temporary dislocation or the start of a more persistent “Europe out-hawks the Fed” phase. With oil volatility still the dominant macro input, the most important swing factor for FX is whether the conflict-driven energy premium remains embedded and whether shipping and LNG disruptions worsen or stabilize; any renewed spike in Brent back toward the 120 area would intensify Europe’s inflation problem and keep markets leaning toward a more restrictive ECB path, sustaining EUR resilience even in a fragile risk backdrop.

At the same time, U.S. rates have technically broken higher, and if 10-year yields continue to grind toward the next resistance zone near 4.6%, USD could regain traction—especially against lower-yielders—if the market starts interpreting “hawkish wait” as “higher for longer.” Scheduled Fed speak (including Vice Chair Barr and SF Fed’s Daly) will be watched for hints on how policymakers are balancing inflation persistence against conflict uncertainty, while flash PMI readings on Tuesday, new home sales, and weekly jobless claims will offer a timely read on whether higher energy and tighter conditions are already squeezing activity.

Equity positioning looks fragile with the Dow hovering above the psychologically massive 45k support zone; a decisive break could trigger a deeper deleveraging episode that would likely restore classic liquidity demand for USD and JPY.

For now, the base case remains a market dominated by oil and policy divergence: Europe’s inflation vulnerability continues to underpin EUR and CHF, while USD’s path depends on whether we get “peak fear” escalation that forces a global dash for liquidity, or a steadier grind where the ECB’s forced-tightening narrative keeps the Dollar on the defensive despite elevated yields.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.