Wall Street ended the week lower as the "dual shock" of surging energy prices and climbing Treasury yields signaled that 1970s-style stagflation is transitioning from a tail risk to a central market theme.

Geopolitical tensions remained the primary catalyst, with US Secretary of State Marco Rubio informing G7 counterparts that hostilities between the U.S./Israel, and Iran are expected to persist for another two to four weeks.

While the administration’s 10-day tactical pause on striking Iranian energy infrastructure was framed as a window for diplomacy, markets interpreted it as a "slow-boil" escalation, especially as Iran restricted access to the Strait of Hormuz for vessels linked to the U.S. and its allies. This "war of attrition" has effectively operationalized a structural supply shock, pushing WTI back above $100 and Brent toward $110.

Unlike typical crises where bonds act as a haven, Treasury yields surged to multi-month highs, with the 10-year hitting 4.48%—its highest since July 2025—as inflation fears began to overwhelm traditional risk aversion. Equity markets buckled under the weight of higher discount rates and the "policy paradox" facing central banks; the tech-heavy Nasdaq slid 3.2%, and the S&P 500 lost 2.1%, while the Dow fell 0.9%, closing precariously near the critical 45,000 support level.

Even President Trump’s unveiling of a high-profile tech advisory panel featuring the CEOs of Nvidia, Meta, and Oracle failed to stem the tide, as investors focused on the fear of $120 oil, 5% yields, and cracking equity floors.

The message from the tape is clear: the era of "Burns’ failure" is over, and today’s central banks appear willing to engineer a "recession light" to prevent inflation from becoming entrenched, leaving the Dollar to emerge as a global "wrecking ball" supported by energy independence and a hawkish Fed.

Pairs In Focus

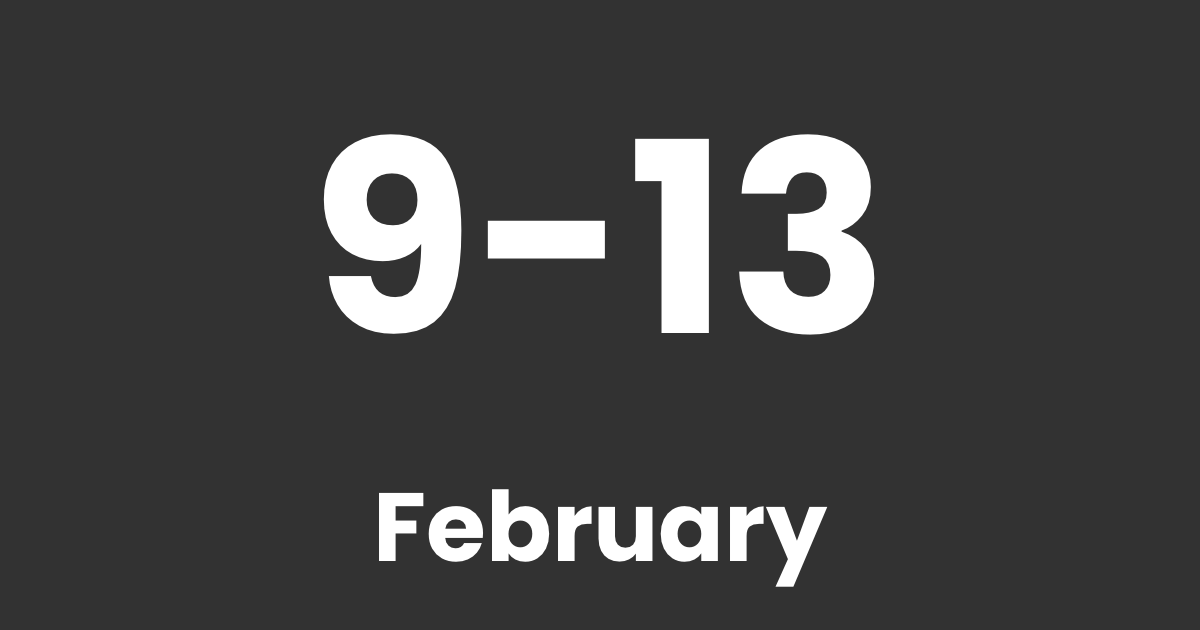

1.AUD CAD

The Australian dollar has shown signs of weakness after a stellar start to the year. The commodity-currency has pulled back, putting a strong support zone around 0.94500 on the radar.

AUD/CAD Daily Chart, Source: TradingView

If price dips and conclusively closes below that level, there is a high risk of a further dip down toward 0.92500.

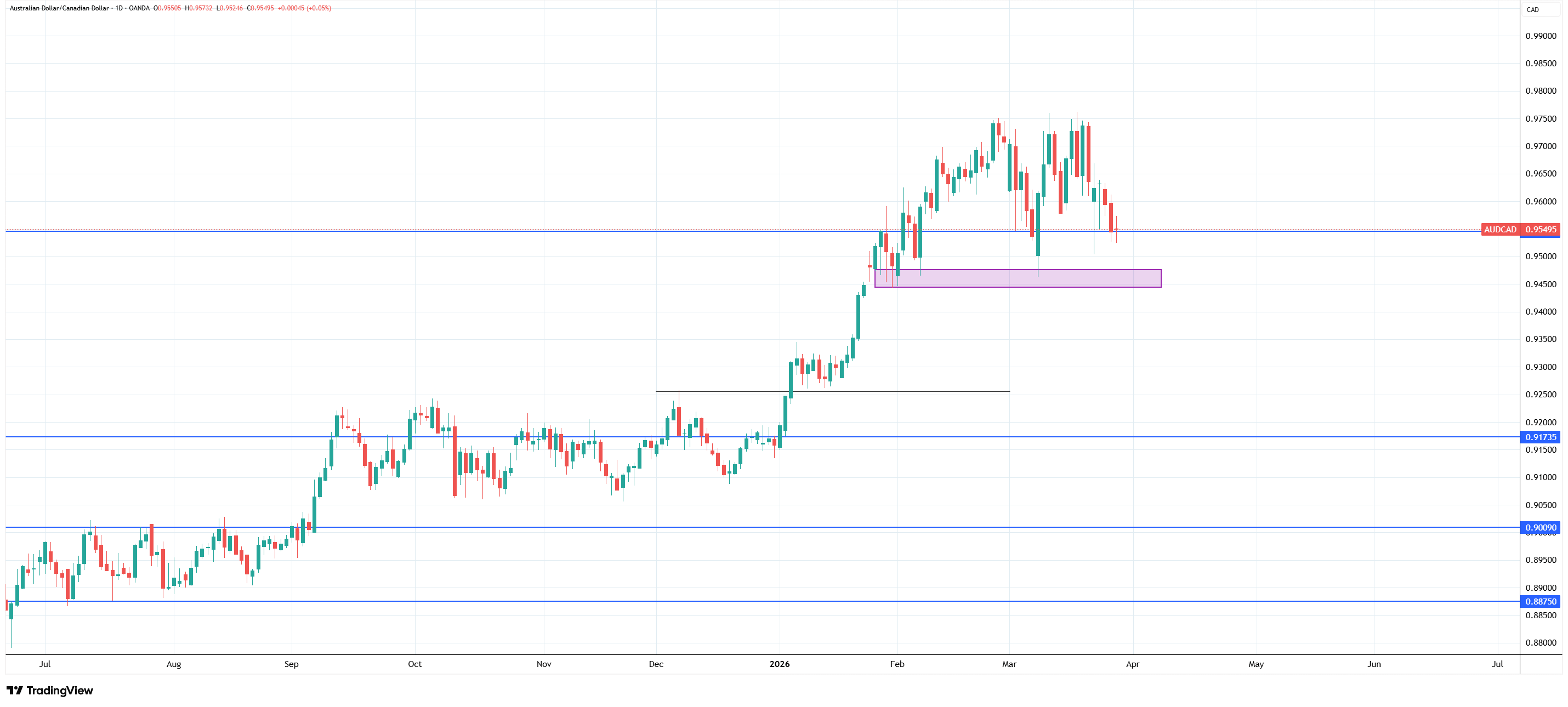

2.GBP JPY

The Pound has been recovering against the yen after dipping in February. Yet it remains on shaky legs, particularly as a BoJ intervention looms over the market.

GBP/JPY Daily Chart, Source: TradingView

The marked trendline is a key observation point, as its break wouldn’t be unusual; however, the retest following the break could indicate the market's direction.

The Week Ahead

The coming week will be a high-stakes test of whether this stagflationary regime triggers a systemic repricing or finds a temporary floor. The market is now laser-focused on the "triple threat" inflection points: a move in Brent toward $120, the Dow breaking below 45,000, or the 10-year yield approaching 5%.

Any of these would likely signal a transition from tactical volatility to a broader shock and institutional deleveraging. Investors will be parsing incoming data and Fed commentary for signs that the "hawkish hold" is shifting toward active tightening. Fed Chair Jerome Powell’s Monday speech might provide clarity on that.

In Europe, the pressure is even more acute; with the ECB facing an asymmetric energy shock, expectations for April and June hikes are firming, which may continue to support the Euro even as regional growth prospects dim. Until energy flows stabilize or inflation expectations are re-anchored, the path of least resistance for risk assets remains lower, while the Dollar and energy-linked inputs are poised to remain the dominant beneficiaries of this new macro regime. The market will be closed on Friday for Good Friday, although the NFP report will still be released.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.