The Dollar ended last week on firmer footing but still trapped within a broader corrective downtrend, as markets juggled a tech-led equity selloff, softer U.S. labor data, and shifting central bank expectations. ADP private payrolls rose just 22K versus 45K expected, while announced job cuts hit their highest January level since 2009, showing that the U.S. labor market is losing some momentum even if it is not yet cracking.

That combination cooled the more aggressive “higher for longer” narrative without fully reviving hopes for rapid Fed easing. In FX, the Dollar benefited intermittently from midweek risk aversion as the tech complex came under renewed pressure, but those gains faded as equities stabilized and the Dow pushed through the 50,000 level for the first time, supported by a powerful rebound in Nvidia and other chip names. DXY extended its rebound off the 95.55 low and broke back above the 97.74 pivot, bringing the 55‑day EMA zone near 98.3 into view as a key decision point.

A failure there would argue the move is just a corrective pause within a larger structural decline, with scope for a renewed push toward 95.55 and, below that, the 91.8 area. Against this backdrop, the Australian Dollar emerged as the strongest major, driven by a clearly hawkish RBA that has shifted decisively back into inflation‑fighting mode.

Rate markets are now leaning toward at least one further RBA hike, giving AUD a robust yield cushion. At the other end of the spectrum, Yen remained the weakest currency, as fading intervention fears and anticipation of a strong mandate for Prime Minister Sanae Takaichi in today’s snap lower‑house election encouraged renewed carry trades. AUD/JPY captured this divergence most dramatically, breaking to fresh record highs above 110 as markets priced in tighter RBA policy and looser Japanese financial conditions anchored by expansionary fiscal plans.

Pairs In Focus

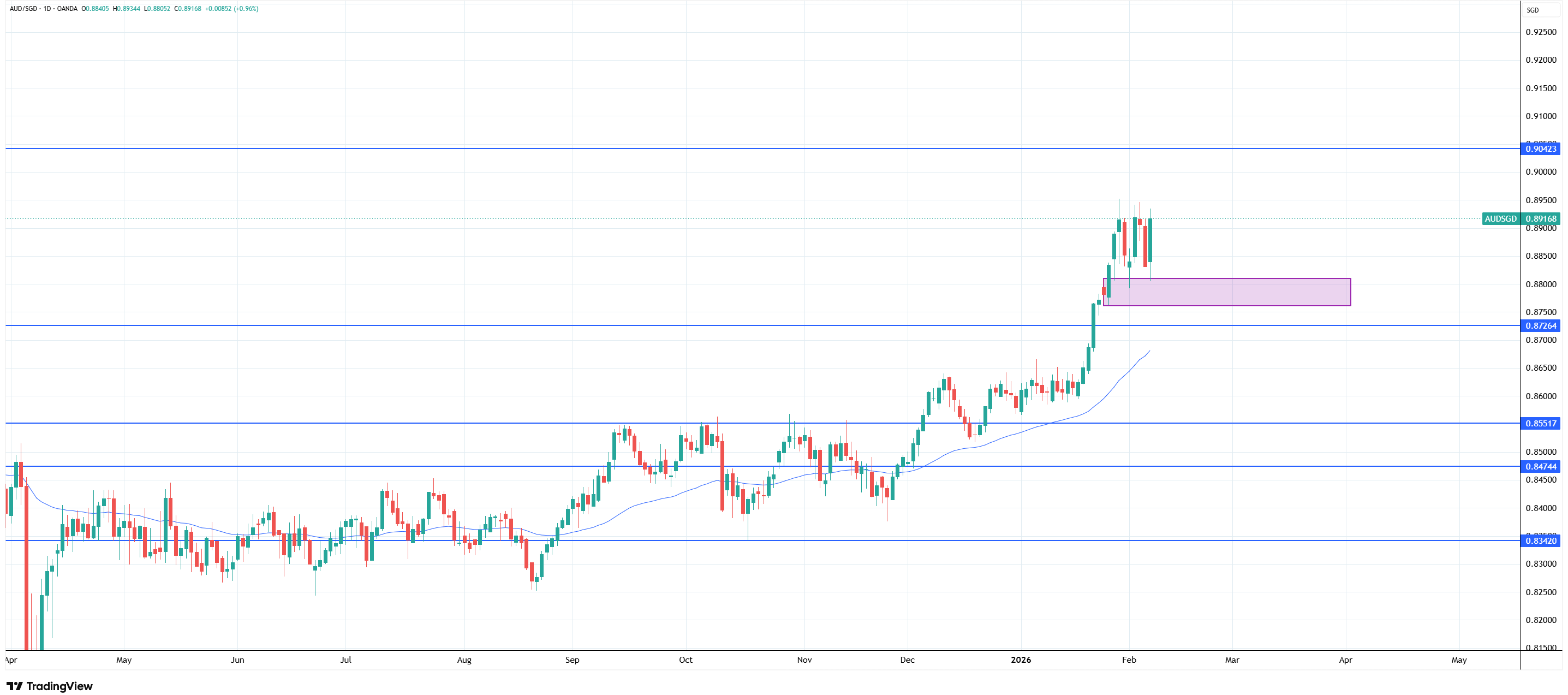

1.AUD SGD

This pair has tested and rejected the support around 0.88. Price action suggests a flag formation that, if it breaks the 0.89500 resistance, could move nearly 200 pips higher.

AUD/SGD daily chart, Source: TradingView

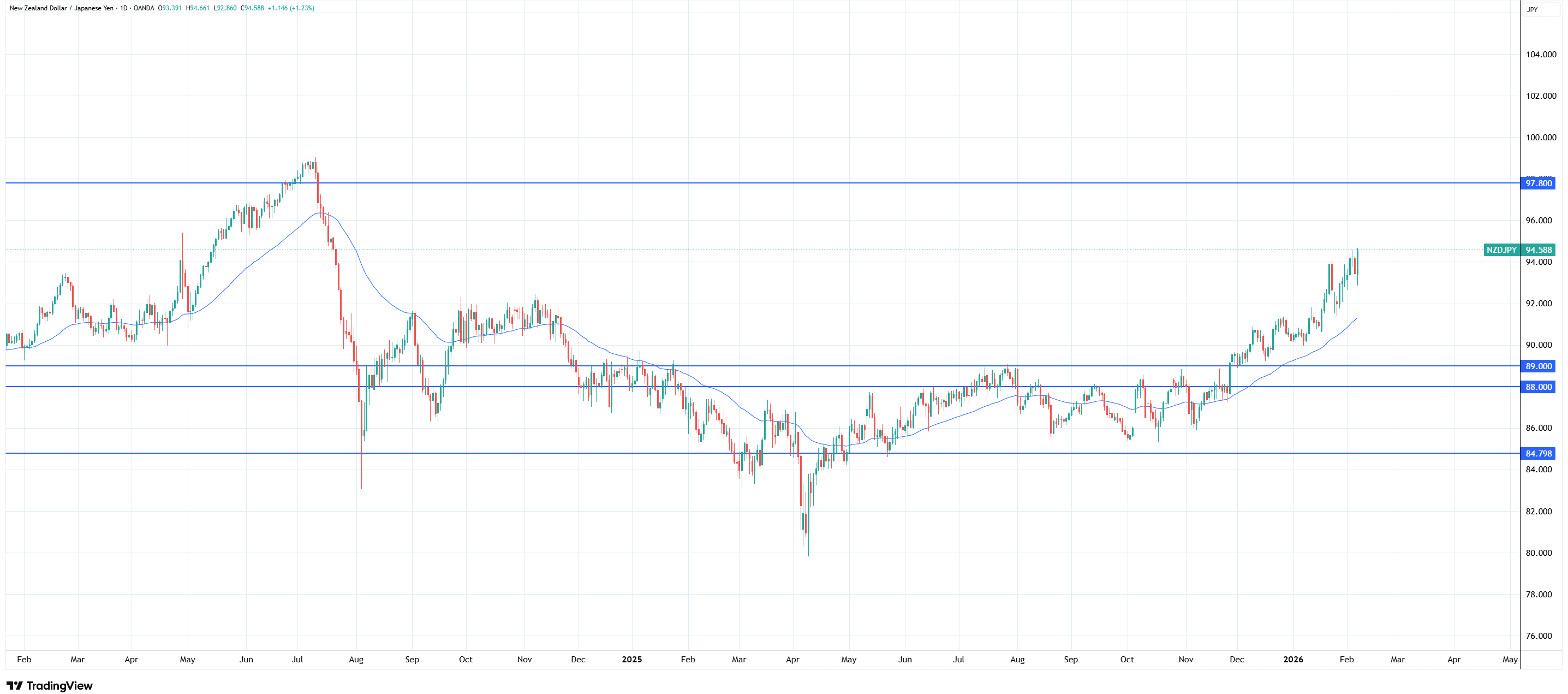

2. NZD JPY

The New Zealand dollar continues to create higher highs and higher lows against the yen. As long as the price keeps above the 92 level, any further dips represent an opportunity to position long with a target of 97.800 in mind.

NZD JPY daily chart, Source: TradingView

The Week Ahead

The coming week will test whether the Dollar’s rebound can extend or stall below its moving‑average ceiling, with U.S. retail sales, a delayed January jobs report, and the delayed January CPI all set to land in quick succession. Any combination of soft consumption and cooling employment would likely cap DXY and favor further upside in high‑beta FX such as AUD, especially if the RBA’s hawkish message is reinforced in local data. Conversely, a resilient U.S. consumer alongside sticky inflation would keep the Fed on hold longer and could drive DXY through the 55‑day EMA toward the 100 area, squeezing shorts particularly against Yen.

For JPY, today’s Japanese election is pivotal. Exit polling suggests the Liberal Democratic Party (LDP)‑led coalition is on track for a win, thus keeping the BoJ cautious about tightening.

It is a mix that structurally weakens the yen but also raises the risk of occasional sharp squeezes if Japanese equities stumble. In that environment, AUD/JPY is likely to remain a key barometer of global risk appetite and relative policy divergence; sustained trading above 110 would keep 113.4 and even the 116–117 region in play over the medium term.

Overall, the Dollar, Aussie, and Yen enter the week at an inflection point where incoming U.S. data and the election outcome in Japan will determine whether recent trends—Dollar stabilization, AUD strength, and JPY underperformance—gain a second wind or start to mean‑revert.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.