The US Dollar Index closed last week under pressure but not in a collapse. The price mostly stalled the prior rebound, as broad but uneven selling prompted its underperformance. Still, it was stronger than the chronically weak Japanese yen.

Markets saw choppy risk sentiment, with divergence between asset classes. Tech and AI-related equities sank, while more traditional and value-oriented sectors fared better. This mix kept high‑beta FX supported but stopped short of a classic “risk‑on” capitulation in the Dollar.

Under the surface, the most important development for currencies was the sudden repricing in U.S. rates, with 10‑year yields snapping higher after briefly testing key technical support. The shift was driven less by data and more by policy‑risk reassessment around the future Fed leadership and the durability of the easing cycle.

For FX, that move injected doubt into the clean bearish USD narrative that had been building. Elsewhere, policy divergence remained the dominant theme. The Swiss Franc stayed bid after the SNB leaned against premature easing expectations. Euro gained primarily on Dollar weakness rather than any improvement in its own macro story.

While the New Zealand Dollar did fine, supported by relative central bank hawkishness, the Aussie lagged on softer labour data and fading rate hike pricing. The British pound traded lower on weak growth data and a more vulnerable domestic backdrop.

Pairs in Focus

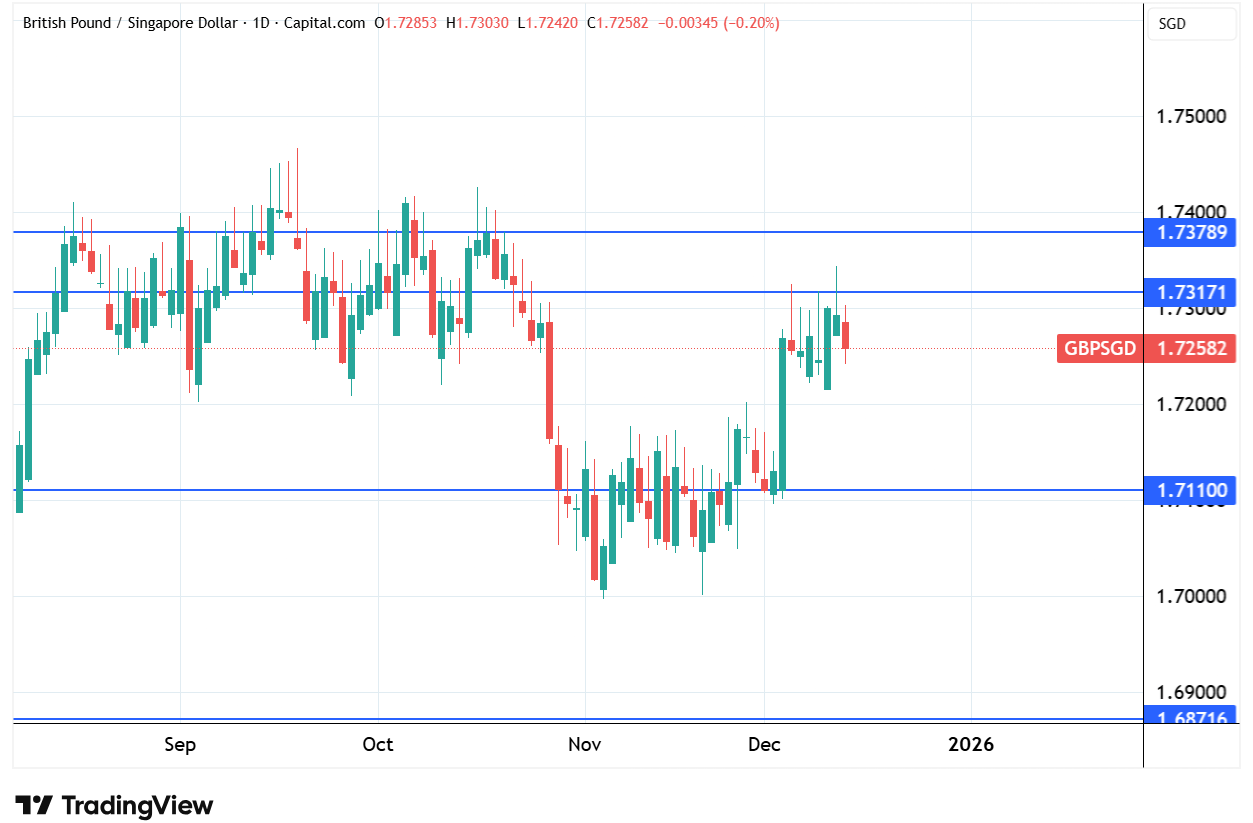

1. GBP SGD

This pair rallied after breaking out of the tight consolidation that occurred through most of November. Yet, after reaching a key level at 1.73170, it failed to sustain its momentum.

GBP SGD daily chart, Source: TradingView

The trend is now at risk of a fadeout and a correction to the lows of the last month. This thesis is more likely to play out as long as the price doesn't close above the previous high on the daily chart.

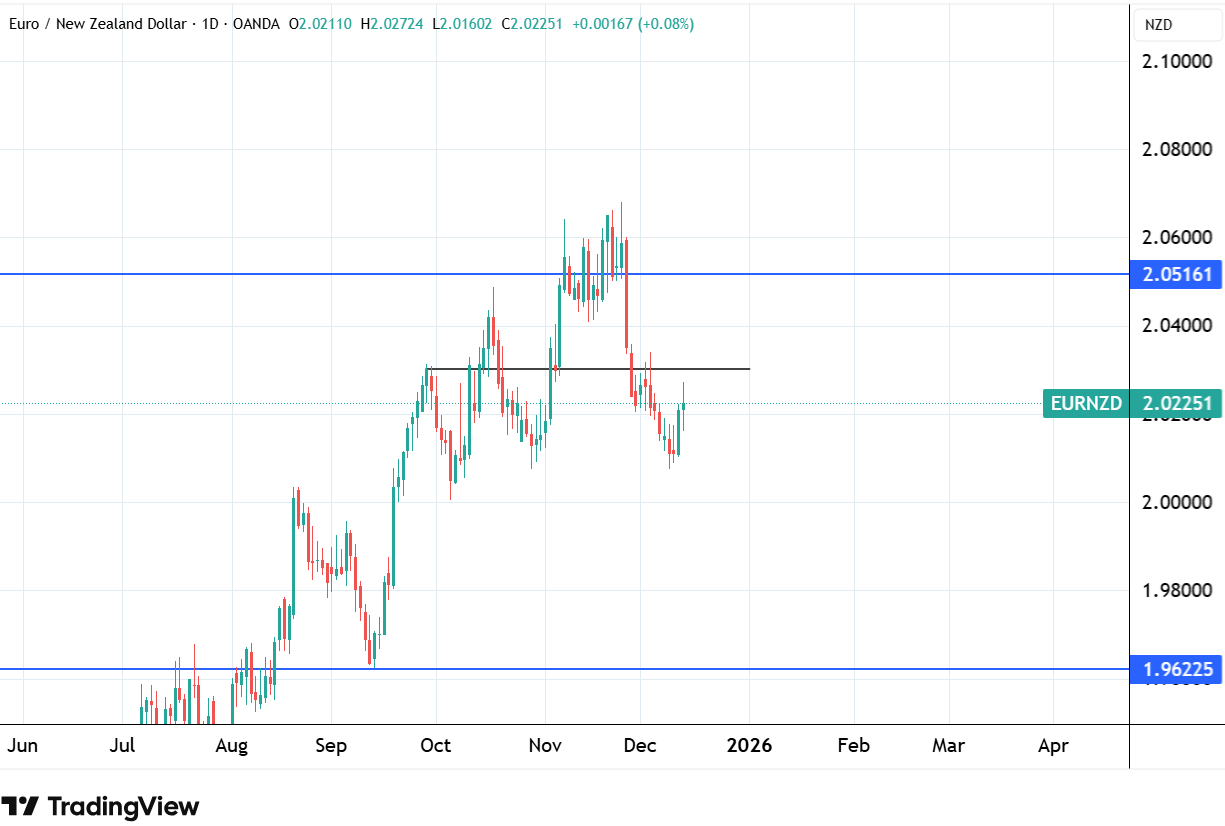

2. EUR NZD

After a significant pullback from the year's highs, this pair found support at the October lows.

EUR NZD daily chart, Source: TradingView

Still, an overall trend remains bullish. Particularly if the price manages to overcome a short-term resistance at 2.0303. In that case, a potential for a spike toward a key level of 2.05160 would be an opportunity.

The Week Ahead

The focus will be on observing whether the U.S. yields can sustain last week’s rebound. A durable break higher in 10‑year rates would provide the Dollar with a floor and could trigger position‑squaring among crowded shorts, particularly against the Euro and the Swiss Franc.

Failure of yields to follow through would revive the broader USD downtrend and support high‑beta FX. Data‑wise, U.S. inflation and labour‑market releases will primarily show how far they validate or challenge the recent repricing of the Fed path. The Bank of England is expected to cut by 25 bps, the Bank of Japan to hike by 25 bps, while the consensus is for the ECB to stay put at 2.15%.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.