After a brief pullback, the US dollar ended the week softer again, as U.S. inflation and a strong equity market rally recalibrated risk appetite. September CPI undershot consensus on both headline and core measures, with the core component rising at its slowest pace since June. Thus, fed fund futures moved to reflect an almost guaranteed 25 bps cut at next week’s FOMC meeting, and likely one more cut by year-end.

The US dollar's repricing propelled commodity currencies. NZD, AUD, and CAD all marked gains. Conversely, JPY weakened sharply as equities rallied and rate volatility eased, while CHF and GBP softened amid a broader rotation into cyclicals. Furthermore, the downside UK inflation surprise reinforced the Bank of England’s easing expectations as the pound rally faded. Euro finished mid-pack, struggling for sustained upside given tepid eurozone growth, but finding some support from the softer US dollar.

Cross-asset moves reinforced the FX narrative. Wall Street logged its best week since early August, with the S&P 500, Dow, and Nasdaq advancing 1.9%, 2.2%, and 2.3%, respectively, aided by strong prints from Tesla and legacy autos, offsetting a Netflix stumble tied to one-off expenses. Progress toward a Trump–Xi meeting and constructive high-level talks in Asia reduced trade tail risk, compressing credit spreads and supporting cyclicals. Meanwhile, Japanese equities surged to fresh highs on political clarity, while the yen’s decline amplified exporters.

Pairs In Focus

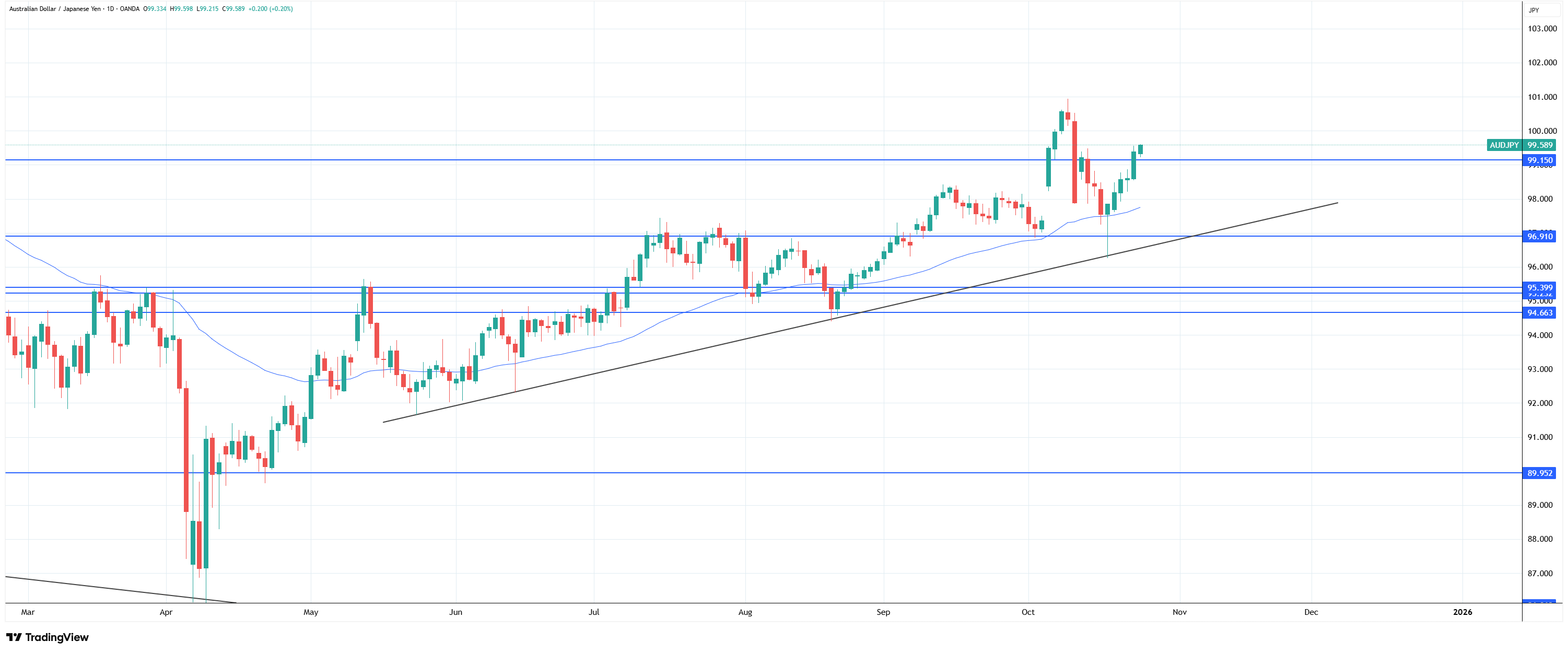

1. AUD JPY bullish

After tagging the lower trendline, AUD JPY surged as expected; however, it has yet to take out the previous high.

AUD JPY daily chart, Source: TradingView

Since the price broke the previous key level around 99.150, the upper near target is 101, while the target above that sits at 102.400

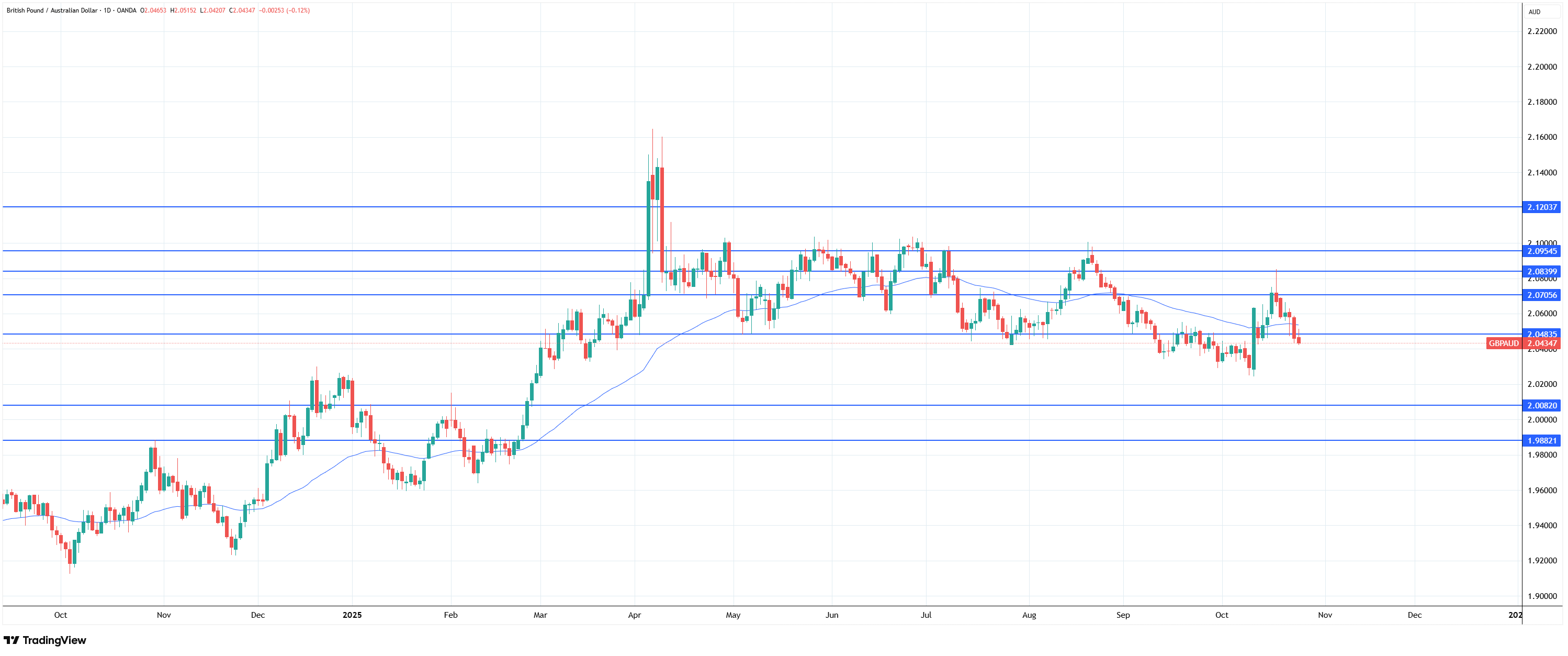

2. GBP AUD

The pound has weakened amid better-than-anticipated inflation, which suggests greater leeway for an interest rate cut.

GBP AUD daily chart, Source: TradingView

Technically, the price has broken a key level of 2.04835. It rejected the retest and, confirming the lower high, it might now push to make a lower low.

Looking Ahead

The spotlight is on the FOMC, as Wednesday’s decision is widely expected to favor a 25 bps cut. Additionally, the central bank will provide the latest guidance on the balance sheet, and the reaction will set the tone for the dollar. A dovish cut with an emphasis on growth risks is likely to extend support for AUD/NZD/CAD and to pressure JPY/CHF; any pushback on December easing could lift USD broadly.

Traders will watch Trump’s Asia trip and the confirmed Trump–Xi meeting for tariff signaling. Furthermore, Trump’s potential meeting with Canada's PM Mark Carney and a trade-deal discussion have not yet been ruled out. It is important to note that Europe has moved clocks one hour ahead to Winter time. This one-week discrepancy with the US means that the London/New York overlap will be on a different schedule for a week.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.