The financial market experienced a choppy, yet ultimately positive week as the US ended a record-long government shutdown. After 43 days, the spending bill finally passed, clearing the way for the resumption of official data.

The Bureau of Labor Statistics quickly confirmed that the long-delayed September nonfarm payrolls report will be released on Thursday, November 20, giving traders a fresh anchor after weeks of trading in the dark. On the other hand, Fed officials, including Cleveland’s Beth Hammack and Boston’s Susan Collins, pushed back against expectations for further rate cuts, arguing that the absence of data does not justify easier policy.

Policy and politics also shaped sentiment. President Donald Trump moved to exempt key food items such as coffee, cocoa, and beef from his reciprocal tariffs, a nod to mounting consumer frustration over grocery prices.

The risk aversion pushed USD/JPY higher and boosted the Swiss franc. Meanwhile, the Australian dollar and the British pound lagged this strength.

Pairs In Focus

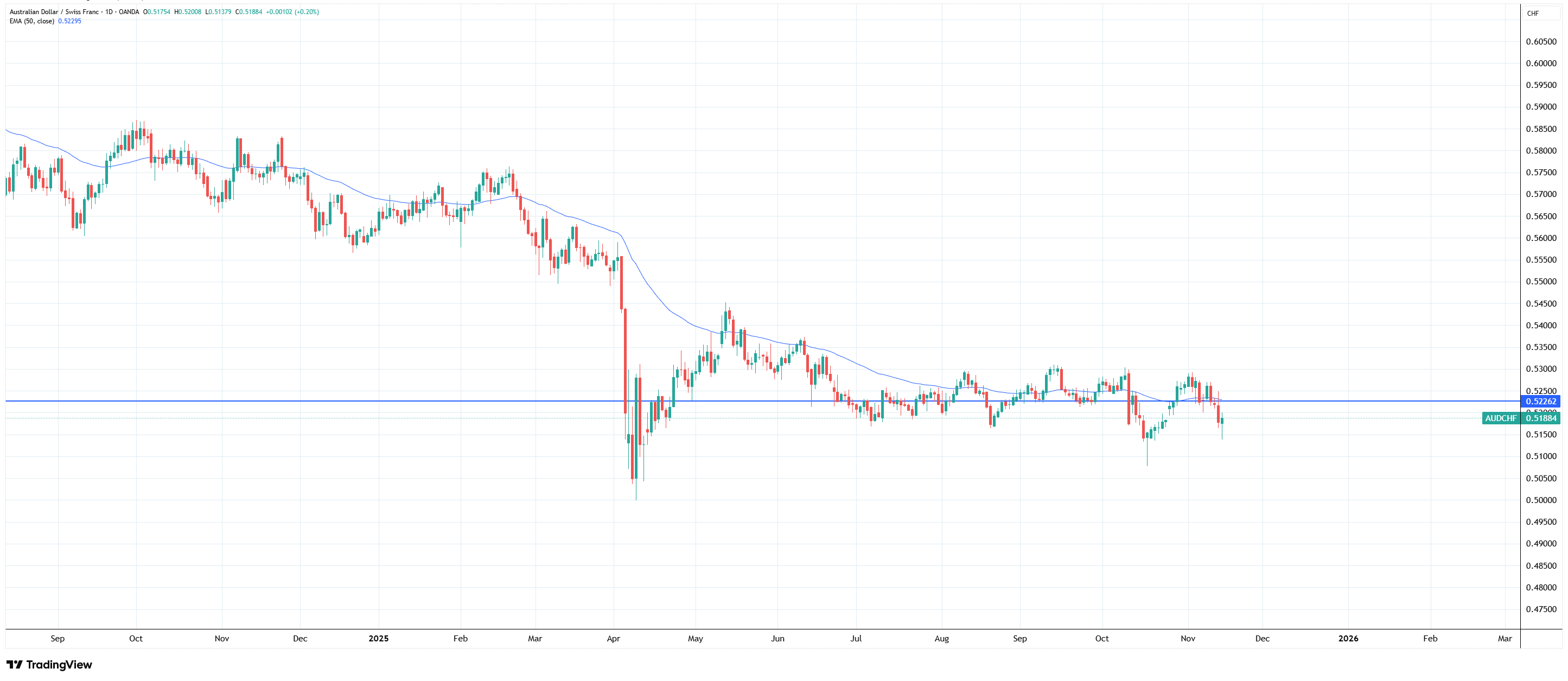

1. AUD CHF

This pair has been lingering around the key level of 0.52260 since late June. However, it has shown signs of weakness, creating a lower low in October.

AUD/CHF Daily chart, Source: TradingView

As long as this level holds, the probability of a continuation lower is growing - particularly if a rally from early November confirms as a lower high.

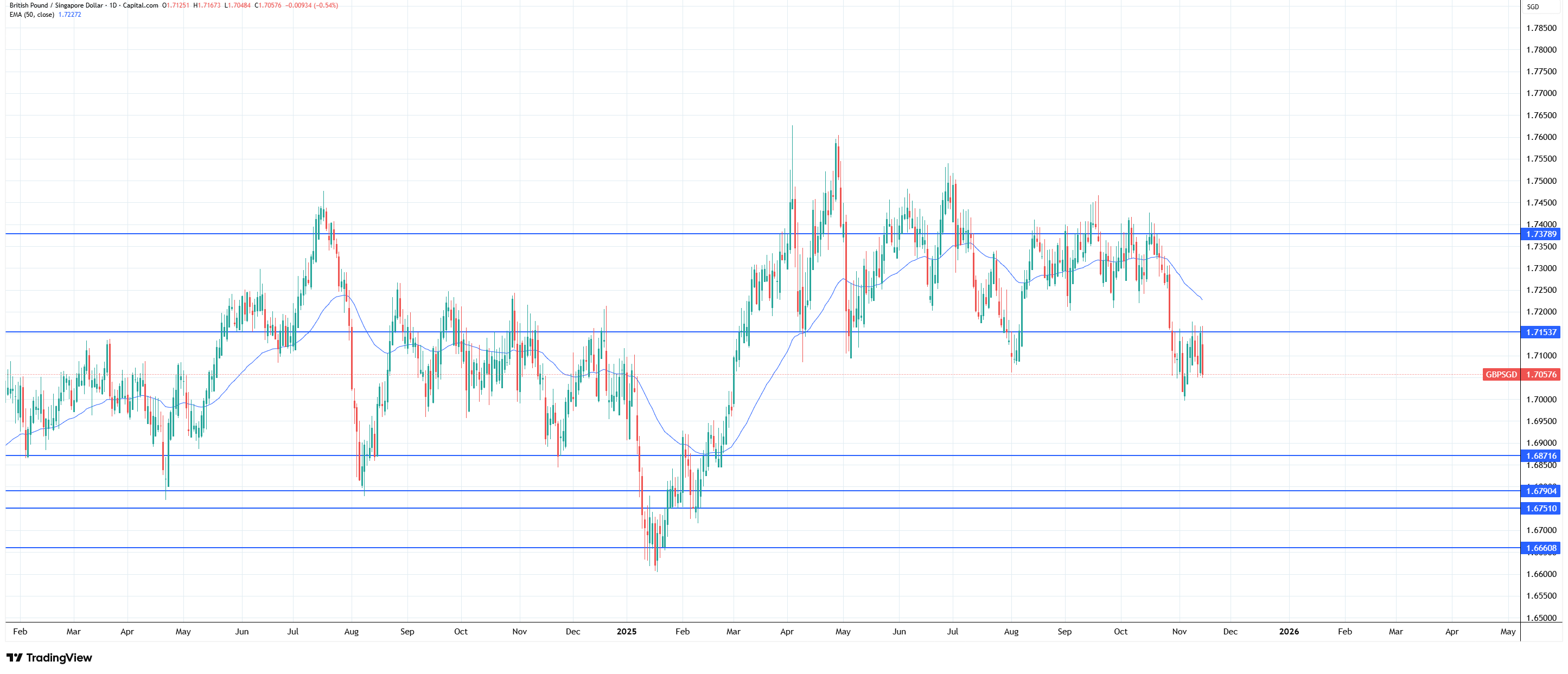

2. GBP SGD

This pair is respecting the previously mentioned level of 1.71500. The price has now tried to retest on 3 occasions, failing every time.

GBP/SGD Daily Chart, Source: TradingView

As long as it stays below, the probability is for the price to move toward 1.68700.

The Week Ahead

The week ahead will be a big test for the equity market. The most valuable firm in the world, Nvidia, will release its quarterly report on Wednesday. The earnings event became a de facto macro catalyst given the stock’s outsized weight and symbolic role at the center of the AI boom.

Any hint of slower data center demand or more cautious capex guidance could deepen the sector’s valuation reset. On the other hand, another blowout print could stabilize sentiment and spark short covering across semiconductors and mega-cap tech.

Equally important, the return of the standard economic calendar will refocus markets on fundamentals after weeks of noise and reliance on surveys. The delayed September nonfarm payrolls report on Thursday will dictate expectations for the Fed’s 2026 interest rate plan. A solid but cooling labor print would support the soft-landing narrative, while a downside surprise could reignite growth worries and favor defensives over cyclicals.

Globally, investors will monitor the lingering risk-off tone in tech, persistent crypto weakness, and evolving rate-cut expectations in the U.K. and Europe, following firmer gilt yields and improved Eurozone trade data.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.