The global risk appetite waned in the currency market last week as the yen and euro posted gains, while the US Dollar index's rally came to an end. The world’s reserve currency closed the week lower at 99.55, erasing the early week’s rally and then some. Both Australia and Britain’s central banks have held interest rates put, as expected.

Equity markets cracked with major U.S. indexes finishing broadly lower as investors rotated out of high-growth and AI-linked names. The equity weakness was amplified when “Big Short” investor Michael Burry revealed short positions against Nvidia and Palantir.

Although numerous media outlets reported Burry’s billion-dollar bet against the leading tech names, it is important to note that this is an options play. The nominal value of Burry’s position is over a billion dollars, but that doesn’t mean he is risking that much. That would depend on the underlying premium he paid.

With the U.S. government shutdown stretching further, economic releases remained frozen, leaving traders to price psychology rather than fundamentals. Sentiment deteriorated midweek as Goldman Sachs CEO David Solomon warned of a likely 10–20% equity drawdown in the coming future.

Pairs In Focus

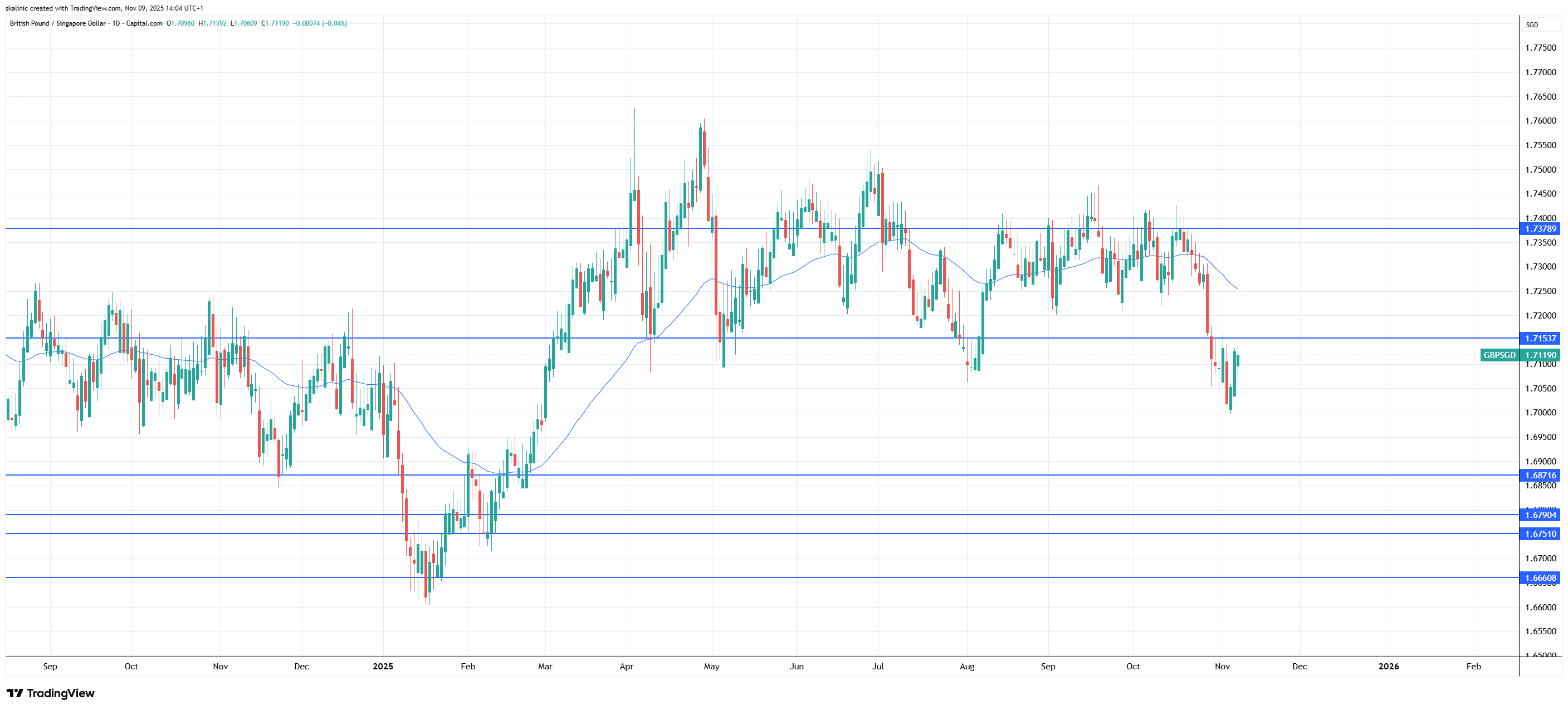

GBP SGD

The Singapore dollar has performed relatively well over the last week, further strengthening against the British pound. Despite a late-week pullback, the market has clearly broken the long-standing market structure, forming a fresh lower low.

GBP/SGD daily chart, Source: TradingView

As long as the daily price persists below 1.71540, the potential for further decline increases.

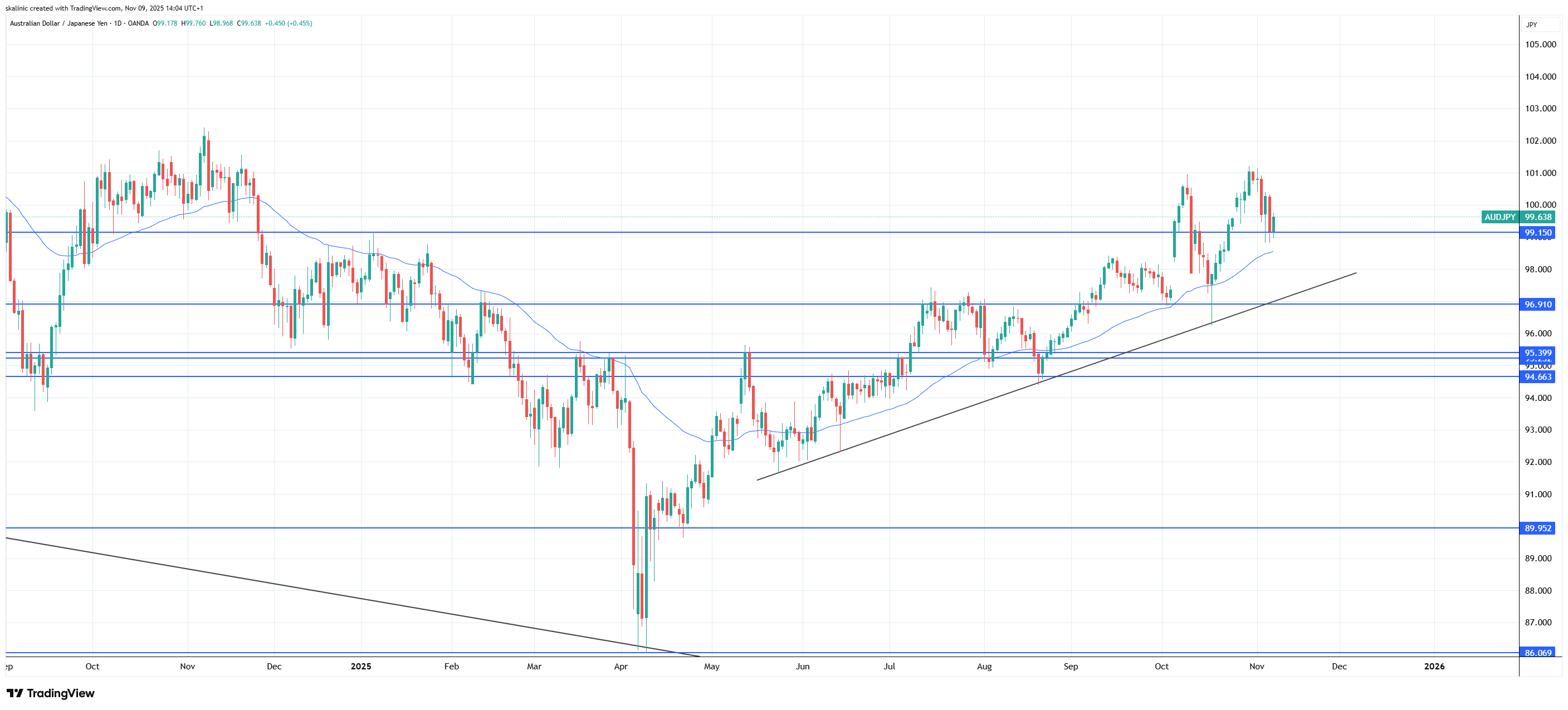

AUD JPY

This pair printed a clear higher high earlier this month, and has since then retraced to support. However, a key level at 99.150 has held firm.

AUD/JPY Daily chart, Source: TradingView

As long as this support continues to hold on a daily basis, the odds of a price moving toward and above 101 grow larger.

The Week Ahead

With the government shutdown, the market remains focused on external data, surveys, and policymakers' comments to gauge sentiment. Third-quarter 13F filings are due Friday, November 14. The disclosures will offer one of the few real data points left to gauge institutional sentiment amid the policy paralysis.

Traders will also brace for headlines from shutdown negotiations, with prediction markets now assigning a better-than-even chance that closures extend past 50 days. Outside of the US, fundamental news about Australian unemployment and the UK’s Claimant Count Change remains the only high-impact news.

Note: Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. Singapore Forex Club is not responsible for any financial decisions based on this article's contents. Readers may use this data for information and educational purposes only.